From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineSteel Market Outlook for Asia: Navigating a Deepening Crisis Amid Surging Chinese Exports

The Asian steel market is grappling with escalating challenges, notably highlighted in the article “OECD Steel Committee warns global steel excess capacity crisis deepens as China exports surge”. This report details a significant contraction in demand alongside notable changes in plant activities, with satellite data reflecting recent operational levels that accentuate these trends.

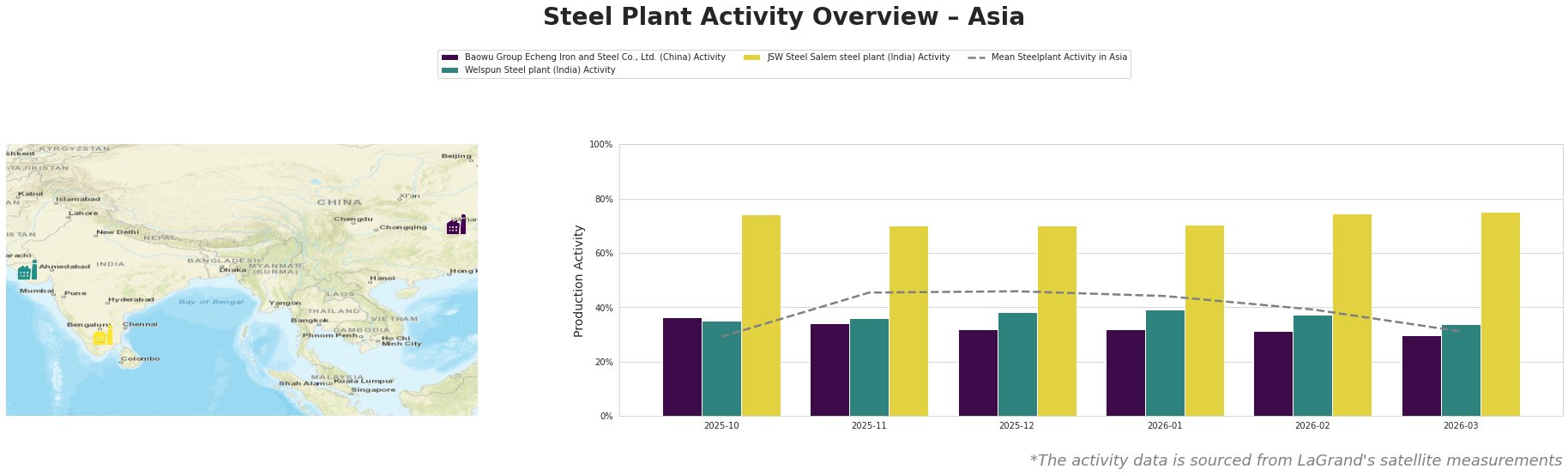

Measured Activity Overview

The mean steel plant activity in Asia shows a decline from 46.0% in December 2025 to 31.0% in March 2026, indicating reduced operational levels across the region. Baowu’s activity fell from 36.0% in October to 30.0% in March, revealing a direct impact amid rising Chinese exports contributing to excess capacity, as noted in “OECD warns of a deepening crisis in the global steel industry”. Conversely, JSW’s Salem plant maintained a comparatively stable level at 75.0%, well above the mean.

Plant Insights

The Baowu Group Echeng Iron and Steel Co., Ltd., located in Hubei, has observed activity drops aligning with the market downturn, decreasing from 36.0% to 30.0% by March 2026. This decline correlates with the OECD’s report of increasing excess capacity chiefly stemming from substantial Chinese production and exports that pressured prices. The plant is reliant on traditional blast furnace techniques, contributing to carbon-intensive productions that are becoming less viable.

Welspun Steel in Gujarat maintained its activity around 35.0% – 38.0%, despite the broader market decline. However, no direct correlation with the OECD’s findings could be established for this plant, as operational steadiness contrasts with neighboring trends.

The JSW Steel Salem steel plant recorded a decline from 74.0% to 75.0%, indicating a robust position relative to peers. It illustrates resilience amid a crisis largely due to its multifaceted operations including DRI and integrated BF processes. This contrasted with depressed demand metrics observed across Asia.

Evaluated Market Implications

Given the current landscape defined by excess capacity reaching 640 million metric tons as per the OECD, buyers should proactively reassess sourcing strategies to mitigate potential supply disruptions. Noteworthy potential pitfalls exist particularly around plants like Baowu, which might face continued operational reductions, threatening supply reliability.

- Buyers are advised to secure contracts with JSW Steel Salem, which has displayed stability and resilience. Its diversified production capabilities may serve as a valuable hedge against the ongoing excess capacity crisis and market instability.

- Monitoring geopolitical developments in the Middle East, as highlighted in the OECD’s insights, will prove prudent for procurement decisions, as escalating tensions could further complicate international steel supply chains.

The interplay of declining demand, rising Chinese exports, and localized operational trends necessitates informed buy strategies tailored to the shifting dynamics of the Asian steel market.