From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineChina’s Steel Market Faces Severe Decline Amid Weak Demand and Rising Costs

China’s steel market is experiencing a Very Negative sentiment, primarily due to decreased production levels highlighted in the article “Murat Eryılmaz: Turkish steel sector faces weak demand and high costs.” The article emphasizes a global downturn in steel output linked to sluggish demand, especially from China. Recent satellite observations of significant activity drops in Chinese steel plants corroborate these findings, showcasing reduced operational efficiency across the sector.

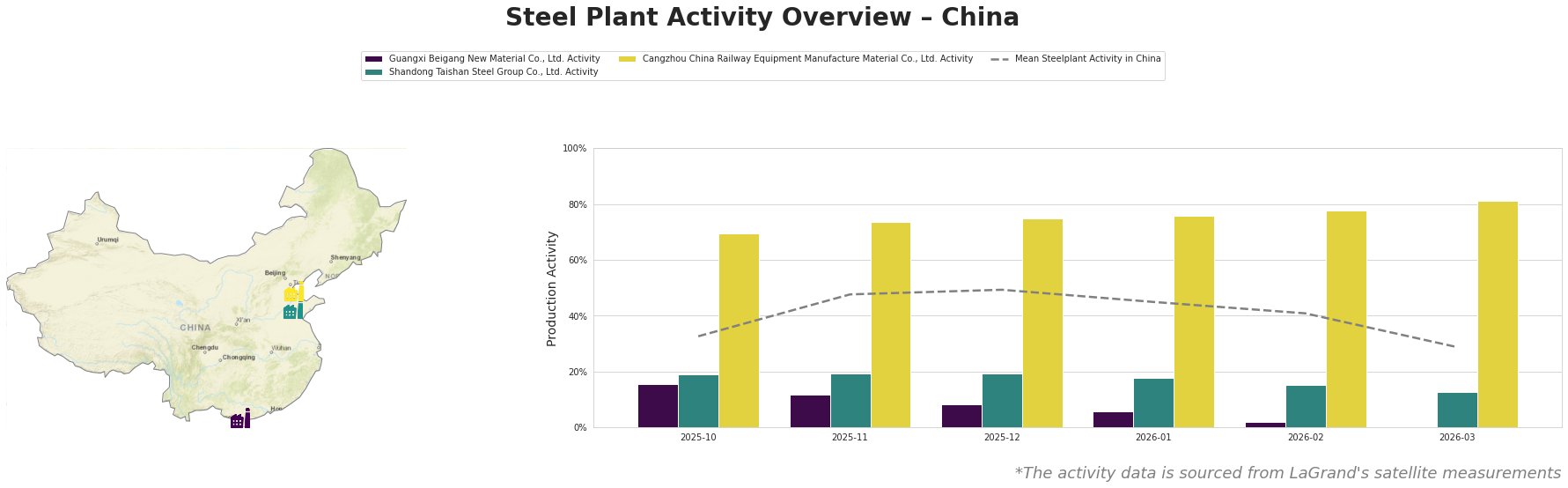

The overall activity in Chinese steel plants showcases a downward trend, dropping from a mean of 33.0% in October 2025 to 29.0% by March 2026. Notably, Guangxi Beigang New Material Co., Ltd. activity plummeted to 0.0% in March, highlighting operational challenges. In contrast, Cangzhou China Railway Equipment Manufacture Material Co., Ltd. remains the highest at 81.0%, suggesting resilience amid broader struggles.

Plant Insights

Guangxi Beigang New Material Co., Ltd.: This facility, with a crude steel capacity of 3,400 tons, primarily utilizes Electric Arc Furnace (EAF) technology. Its activity fell drastically from 15.0% in October to 0.0% in March 2026, coinciding with the noted global production decline in the article. There’s a clear link between reduced operational capacity due to weak domestic demand as discussed in Eryılmaz’s statements.

Shandong Taishan Steel Group Co., Ltd.: Operating at 5,000 tons capacity, the plant has experienced activity resting at 19.0% from October to December, moving slightly lower with 18.0% in January 2026. These reductions echo the overall weakening of demand discussed in the news article, implying a challenging procurement outlook for suppliers and stakeholders.

Cangzhou China Railway Equipment Manufacture Material Co., Ltd.: This plant, boasting a capacity of 7,500 tons, has shown more stability, maintaining above 75.0% activity through early 2026. Despite this resilience, the decrease to 81.0% in March reflects the effects of broader market pressures affecting demand across the steel sector, mandating caution among buyers.

Market Implications

Given the declining activity levels and overall market sentiment, steel buyers should anticipate potential supply disruptions primarily from Guangxi and Shandong plants, where considerable drops in activity raise concerns over operational outputs.

Recommended Actions:

– Short-term Procurement Caution: Buyers should strategize short-term purchases to avoid potential shortages, especially from plants with extreme activity reductions like Guangxi Beigang.

– Supplier Diversification: Assess alternative suppliers, particularly focusing on operations similar to Cangzhou that continue demonstrating operational resilience, but remain vigilant about broader market conditions impacting future availability.

– Monitor External Costs: Be mindful of rising costs as indicated in the article regarding snippets on production expenses, which are likely to impact negotiations and procurement strategies going forward.

Overall, strategies grounded in these insights can help better navigate the turbulent waters of the current steel market landscape.