From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEuropean Steel Market Faces Weak Demand and Activity Declines Amid Rising Prices

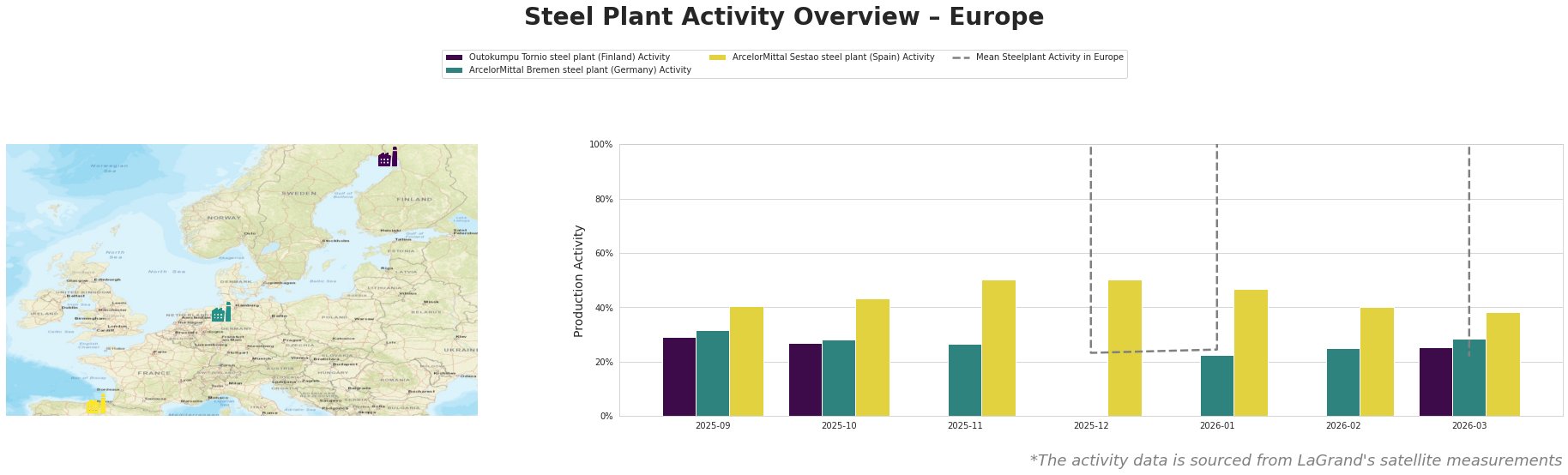

Europe’s steel market sentiment remains negative, primarily driven by weak demand and stagnant plant activity levels. Recent reports, such as “European HRC prices edge higher, but weak demand and near-dead imports curb activity“ (March 12, 2026) and “European HRC prices are rising, and import restrictions continue to affect sentiment“ (March 10, 2026), highlight rising hot-rolled coil (HRC) prices despite a prevailing struggle for producers to sell at increased rates. Consequently, satellite-observed activity for major steel plants has seen notable declines.

Activity at major plants indicates a downward trend, particularly noted in the ArcelorMittal Bremen steel plant, which fell to 28% in March after a notable drop from 43% in October. Similarly, the Outokumpu Tornio plant registered 25% activity, down from 29% previously, corroborating the report’s findings on weakened market dynamics.

Outokumpu Tornio has a production capacity primarily in electric steelmaking and serves various sectors including automotive and infrastructure. The observed decline aligns with industry pressures as stated in “European HRC prices edge higher, but weak demand and near-dead imports curb activity.” The ArcelorMittal Bremen plant, being an integrated producer, showcases reduced activity, correlating with the diminished market interest expressed in the same article.

The ArcelorMittal Sestao plant, while maintaining a higher relative output until recent observations, demonstrated a drop to 38% in March from 50% in November 2025. This shift relates to increasing import constraints and fluctuating energy prices, as highlighted in “European HRC prices are rising, and import restrictions continue to affect sentiment.”

In conclusion, potential supply disruptions are imminent, particularly in plants like Bremen and Sestao, given their reduced operational capacity against the backdrop of heightened market prices and geopolitical tensions. Steel buyers should consider strategically delaying large commitments until clearer demand signals are noted. Procurement strategies should pivot toward hedging against further price increases while engaging with suppliers about competitive pricing strategies below current market offers.