From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineGermany’s Steel Market Faces Headwinds: Price Hikes and Decreased Plant Activity

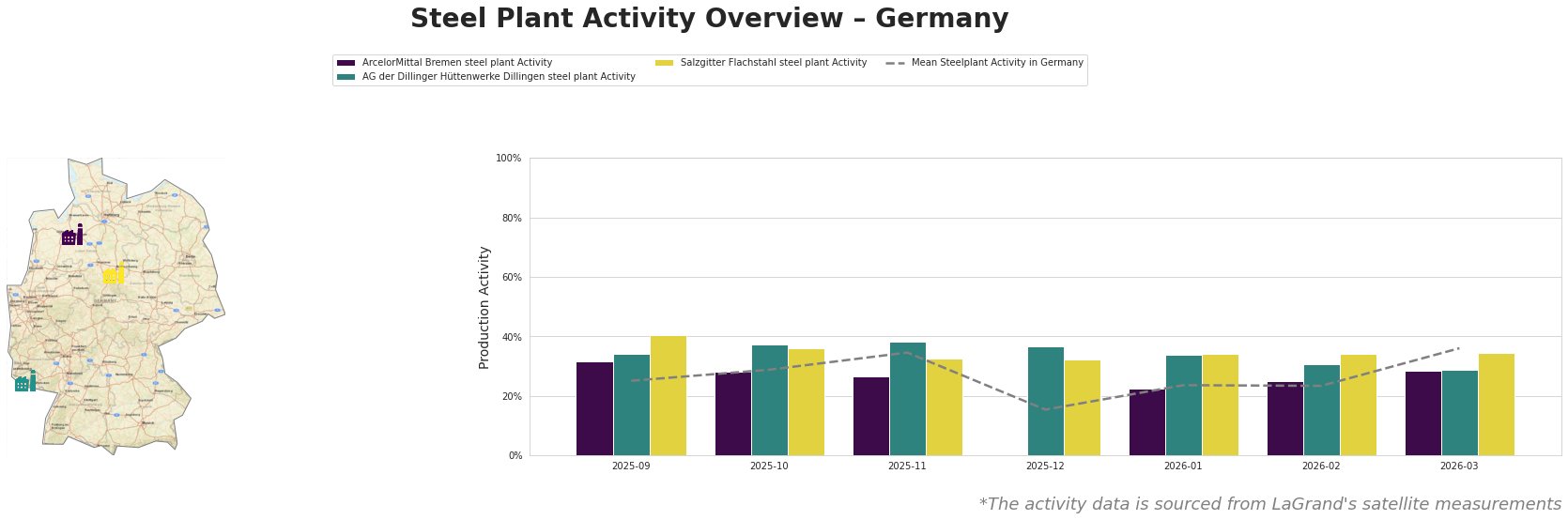

Germany’s steel market is experiencing a negative sentiment, driven by decreased demand and recent price adjustments. Notably, the article NW European Roll forming plants raise prices, distributors hesitate emphasizes that distributors in Northwestern Europe are struggling with increased prices—up by €60 per ton since December 2022—while also facing a lack of consumer demand that may result in further price decreases. This sentiment is reflected in the satellite-observed activity at key steel plants, with activity at ArcelorMittal Bremen dropping from 32% to only 23% in January 2026.

Measured Activity Overview

ArcelorMittal Bremen’s activity has decreased significantly from 41% in September 2025 to 23% in January 2026, aligning with the observed struggles outlined in NW European Roll forming plants raise prices, distributors hesitate. The AG der Dillinger Hüttenwerke has been more stable but saw a marginal decline from 38% in November to 34% in January. Meanwhile, Salzgitter Flachstahl maintained activity around 34%, but this stability is overshadowed by the overall market downturn indicated in the articles.

Evaluated Market Implications

The significant price increases reported in NW European Roll forming plants raise prices, distributors hesitate are unlikely to stimulate demand, given the pressing economic challenges and uncertainty in energy markets as highlighted in European HRC prices edge higher, with import constraints continuing to drive sentiment. The activity drops at ArcelorMittal Bremen, which could face potential production disruptions if demand does not improve, suggest that procurement strategies for steel buyers should focus on negotiating prices closer to €650-660 per ton, as indicated by market resistance. Steel buyers are advised to monitor competitive pricing and remain flexible in their sourcing strategies, particularly around potential volume allocations from AG der Dillinger Hüttenwerke and Salzgitter Flachstahl, as they continue to show elevated activity levels albeit under pressure.

Investing in short-term contracts might mitigate risks during this volatile period, especially given the geopolitical uncertainties affecting the energy landscape and overall supply chain constraints, which could impede access to lower-cost imports.