From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineNeutral Market Sentiment Prevails in Algeria’s Steel Sector Amid Increased EU Quota Exhaustion

Algeria’s steel market faces a neutral sentiment influenced by significant recent developments. As highlighted in the article “EU steel safeguard quotas fill up for Q1, with Turkey nearing exhaustion of HRC quota,” Algeria has completely utilized its Hot-Rolled Coils (HRC) quota for Q1, which reflects growing demand similar to trends observed in the EU market. Correspondingly, satellite data observed various steel plants showcasing fluctuating activity levels, indicating inconsistent operational output.

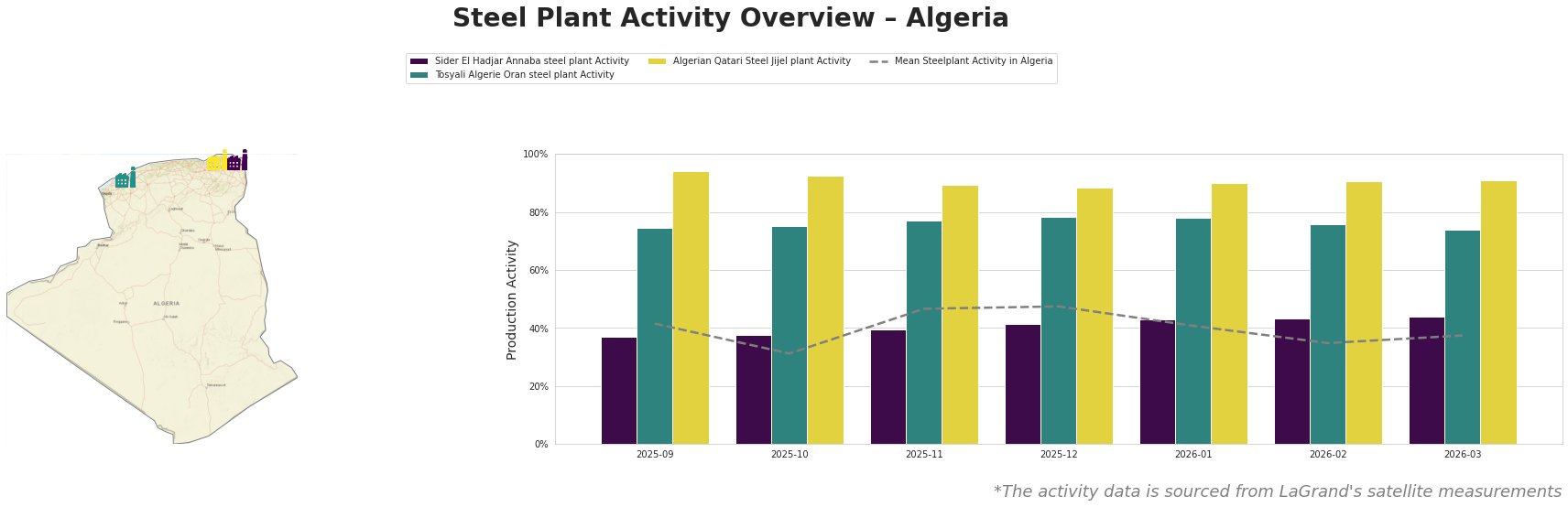

Activity levels across Algeria’s steel plants have shown variability, with the mean activity declining from 42.0% in September 2025 to a recent 37.0% in March 2026. The activity at Sider El Hadjar Annaba rose from 37.0% to 44.0%, suggesting a slight recovery. In contrast, Tosyali Algerie Oran experienced a decline from 75.0% to 74.0%, while Algerian Qatari Steel Jijel remained stable around 91.0%. Notably, the increase in Sider El Hadjar’s activity does not have a clear connection to the EU quota exhaustion reported in the aforementioned article.

Sider El Hadjar Annaba operates at a capacity of 1.8 million tons of crude steel using integrated processes (BF/EAF). Its recent activity rise to 44.0% in March might suggest recovery efforts amidst challenging market conditions, although no direct correlation with quota status was established.

Tosyali Algerie Oran is a DRI/EAF facility capable of producing 3.7 million tons, currently showing a slight decrease in operational activity. The consistency in production at 74.0% implies a controlled output as it navigates international supply chain challenges heightened by heavy demand driven by EU quotas. Again, no links with quota statuses were identified.

Algerian Qatari Steel Jijel has maintained high operating levels, indicative of robust production strategies, with activity levels remaining around 91.0%. While its operations are crucial for meeting local demand, especially as import quotas are exhausted, the connection to EU quota dynamics is unestablished from the data.

These observations suggest potential supply stability through local production. However, buyers must remain vigilant as any fluctuations in demand or unexpected global market shifts could result in constraints. Procurement strategies should consider sourcing from the higher-performing Sider El Hadjar Annaba and Algerian Qatari Steel Jijel to solidify supply chains, particularly for HRC products, given the exhaustion of available quotas. Further assessments may be warranted as the quota impacts and operational trends develop throughout the next quarter.