From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEurope Steel Market Report: Neutral Sentiment Amidst Price Hikes and Regional Disparities

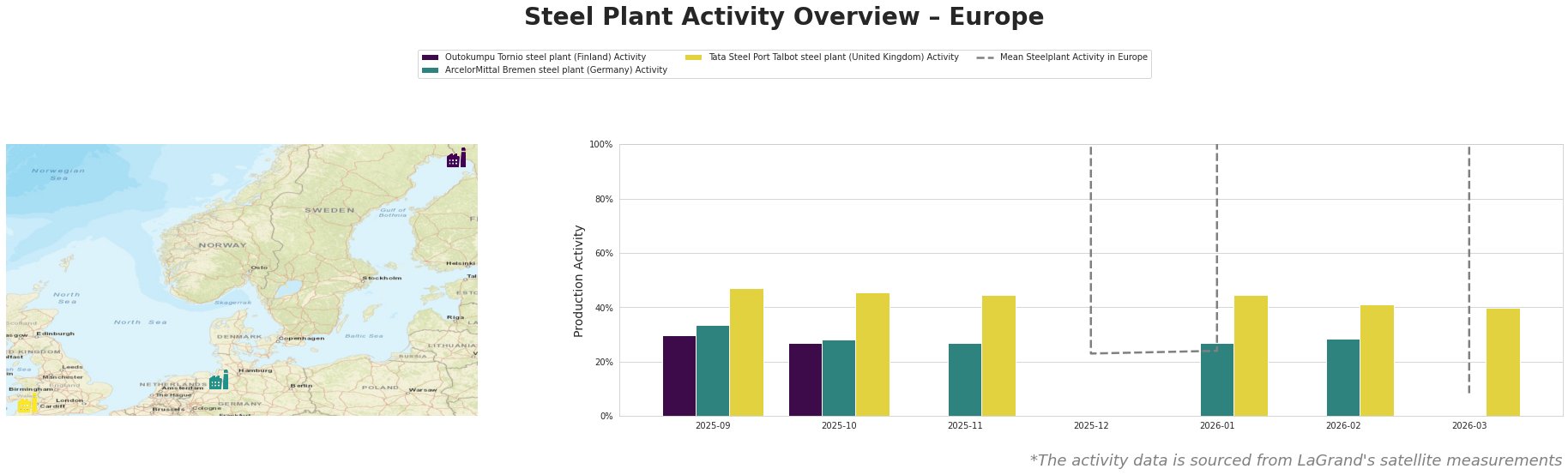

Recent developments in the European steel market reflect a cautious outlook, particularly regarding the responsiveness of distributors to price hikes amidst low demand. As detailed in the article “Distributors slow to capitalise on EU coil hikes“, European mills are incrementally raising prices, with targeting figures of €720/ton, while actual transaction prices linger around €680/ton, complicating distributors’ efforts to adjust. This pricing dynamic is further complicated by satellite-observed activity data indicating fluctuating levels across key plants, confirming the ongoing instability within the sector.

Activity at ArcelorMittal Bremen dipped to 27.0% in November 2025, aligning with the context of rising prices in “UK HRC discount to north EU expands“. This plant’s stable production of hot-rolled and cold-rolled coils reflects related market pressures, particularly due to increased UK imports amid domestic production challenges. Similarly, Tata Steel Port Talbot showcased a slight decrease in activity in early 2026 but remained operationally stable at 41.0% by late February, possibly influenced by the discrepancies in pricing highlighted in the same report.

Outokumpu Tornio, with a significant activity drop to 27.0%, does not show a direct correlation with the recent events captured in the articles, suggesting market-specific dynamics affecting Finnish producers.

Importantly, activity levels are notably below the mean of 43.0% for early 2026, especially when compared with historical averages. The “Coil imports resurface in Italy“ article reveals rising Italian coil prices despite subdued activity, with traders absorbing potential CBAM risks to manage costs effectively. This reinforces the need for strategic procurement as imports may offer price advantages in some regions amid domestic volatility.

Given the observed market activity and news context, steel buyers should focus on procurement flexibility. Specifically, regional imbalances signal potential supply constraints; for example, standing operational challenges at UK plants may necessitate increased sourcing from EU suppliers to hedge against price volatility. Engaging in futures contracts may also be prudent as market dynamics evolve, especially with the expectation of further price adjustments highlighted in the “Distributors slow to capitalise on EU coil hikes”.

In conclusion, the current market sentiment reflects neutrality, driven by balancing price increases against low demand and production challenges. Buyers are advised to leverage strategic sourcing, focusing on regions with more stable supply chains while remaining adaptable to market shifts influenced by import dynamics and regulatory changes regarding CBAM costs.