From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEurope Steel Market Update: Price Increases Amid Stagnant Demand and Regional Disparities

Recent developments in the European steel market indicate a challenging landscape marked by inconsistent plant activities and pricing pressures. Notably, the article “Distributors slow to capitalise on EU coil hikes“ details how European coil mills are struggling to pass on gradual price increases, with service centers selling below sustainable levels. Additionally, the closure of Tata Steel UK’s blast furnace has led to a significant discount in the UK market, as highlighted in both “UK HRC discount to north EU expands“ and “The discount on HRC services in the UK is expanding for the Northern EU countries“. Although some mill activity is declining, the situation remains complex, as illustrated by the “Coil imports resurface in Italy“.

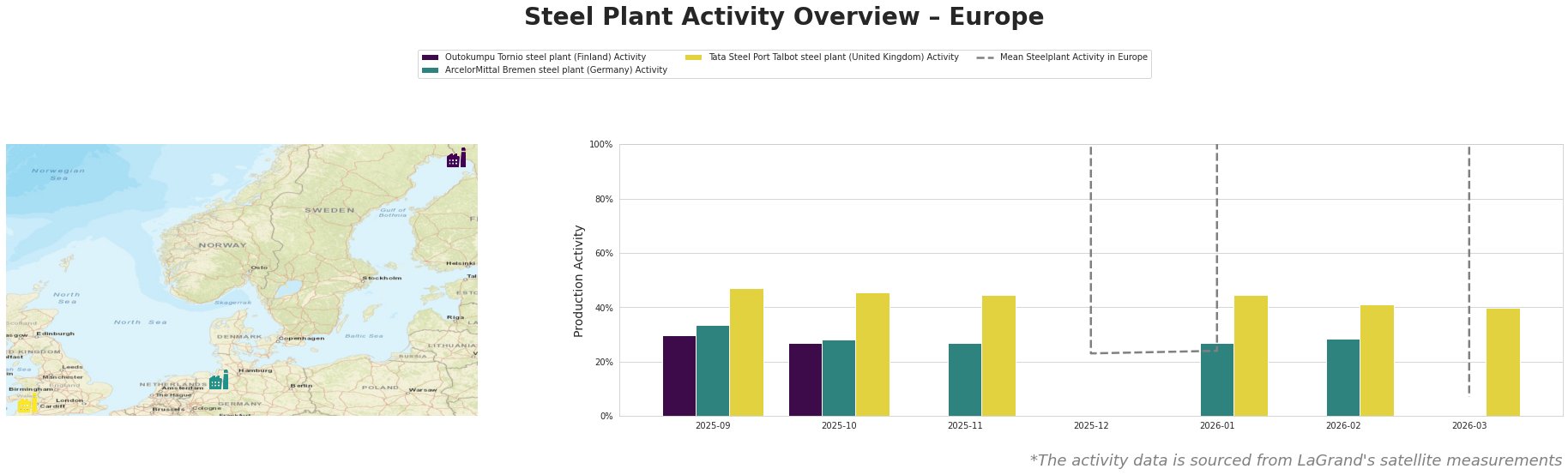

The overall mean activity across all observed plants has declined significantly to 7% by February 2026, with notable drops at Outokumpu Tornio and attempts of recovery at Tata Steel Port Talbot, which reached 40% activity.

At the Outokumpu Tornio steel plant, situated in Finland, activity dropped to 27% in both October and November 2025, severely aligning with the broader downturn in European demand, corroborated by “Distributors slow to capitalise on EU coil hikes”, emphasizing the stalling capacity for distributors. However, this plant displays a stable production capacity of 1.2 million tonnes per year through electric arc furnace technology.

Conversely, the ArcelorMittal Bremen steel plant has shown variability, maintaining 33% in September but dropping to 27% in November, which corresponds with increased local competition and pressure from competitors in the UK.

The Tata Steel Port Talbot steel plant demonstrated relatively high activity levels, hitting 47% in September, largely due to historical operational capacities. Following recent news, including the closure of Tata Steel UK’s last blast furnace, the plant’s activity saw fluctuations, but it remains poised for recovery with 40% activity in March 2026.

This analysis reveals potential supply disruptions, especially for regions like the UK, where pricing strategies may lead to unstable supplies. Steel buyers should consider diversifying procurement channels—especially sourcing from the UK, where discounts of €62 per tonne under north European prices provide an opportunity for cost-effective acquisitions. However, the risks associated with CBAM compliance and the prevailing low domestic demand should be carefully weighed against these pricing opportunities.

To optimize procurement, it’s essential to closely monitor these regional discrepancies and adapt strategies accordingly, especially focusing on leveraging competitive prices in the UK while factoring in the ongoing volatility within the European market.