From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEuropean Steel Market Outlook: Very Positive Sentiment Amid Domestic Production Surge

In Europe, particularly in Italy, recent developments in steel production indicate a robust recovery. Acciaierie d’Italia restarts BF No. 2 and Confectionery “Italy” reopens BF No. 2 signal a strategic doubling of output to 4 million tons per year by April 2026, as European buyers shift focus towards domestic suppliers amid rising import prices due to the Carbon Border Adjustment Mechanism (CBAM). However, maintenance on blast furnace No. 4, beginning on February 28, 2026, may temporarily impact overall production levels.

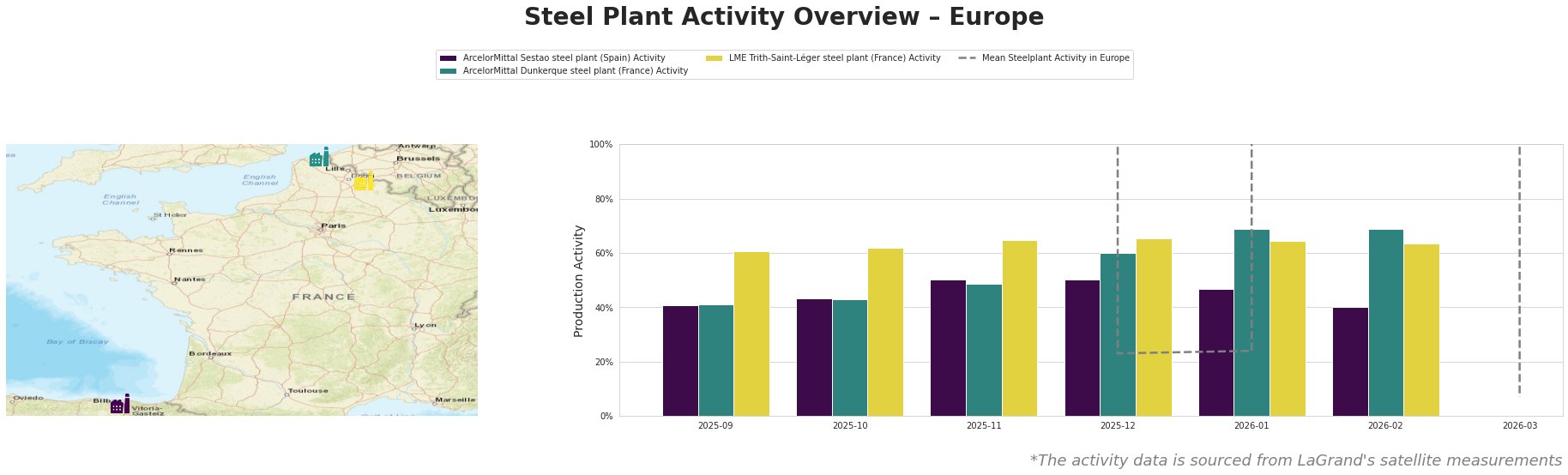

The satellite-observed activity levels show a significant recent decline in mean activity, dropping to 7% in February 2026 from the previous month’s 24%. The ArcelorMittal Dunkerque steel plant is noteworthy, with activity levels holding at 69% amid fluctuating patterns elsewhere. In contrast, the ArcelorMittal Sestao plant dropped to 40% as of February, aligning with other reports without a directly established connection to news developments. Conversely, LME Trith-Saint-Léger remains stable at 64%, but again, no direct connection can be made to recent news.

The activity at ArcelorMittal Sestao, which has a capacity of 2.0 million tons, experienced a notable drop to 40% in February, indicating potential challenges in ramping back up to full production. This decline follows no specific news tie but is critical for steel buyers, as the plant typically supplies hot-rolled coil to the automotive and building sectors. ArcelorMittal Dunkerque, with a larger capacity of 6.75 million tons, saw activity stabilizing at 69%, correlating with high demand for semi-finished products, independent of any specific news. The strategically aligned production levels here are essential for maintaining market supply continuity.

The LME Trith-Saint-Léger’s consistent performance at 64% activity illustrates resilient operation in the low output environment. This plant’s electric arc furnaces convert scrap into finished products and remain pivotal for sectors dependent on sustainable production practices.

Given the current trajectory of domestic production increases, allied with intertwined news about the restarts and maintenance of significant facilities, procurement teams should consider:

- Immediate procurement of product categories from Dunkerque and Trith-Saint-Léger before scheduled maintenance at Taranto commences to hedge against potential supply disruptions.

- Shift purchasing towards ArcelorMittal Dunkerque, as its ongoing high activity level may provide a more stable supply of slabs and hot-rolled products during the fluctuation induced by maintenance events at other plants.

- Monitor developments at ADI closely, particularly during the maintenance period of BF No. 4 starting February 28, 2026, which may influence market dynamics and dictate urgent procurement decisions thereafter.

These insights indicate significant opportunities for procurement decisions that align with local production capacities and strategic market shifts in the European steel landscape.