From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineSteel Market Woes in Africa: Production Suspensions and Declining Activity Signal Peril for Buyers

The steel market in Africa is facing a very negative outlook marked by significant operational disruptions. Notably, Rio Tinto suspends iron ore production at Simandou in Guinea, amid ongoing fatalities, which directly coincides with decreasing activity levels in regional steel plants. The closure has potential implications for iron ore availability, contributing to a dampened production environment.

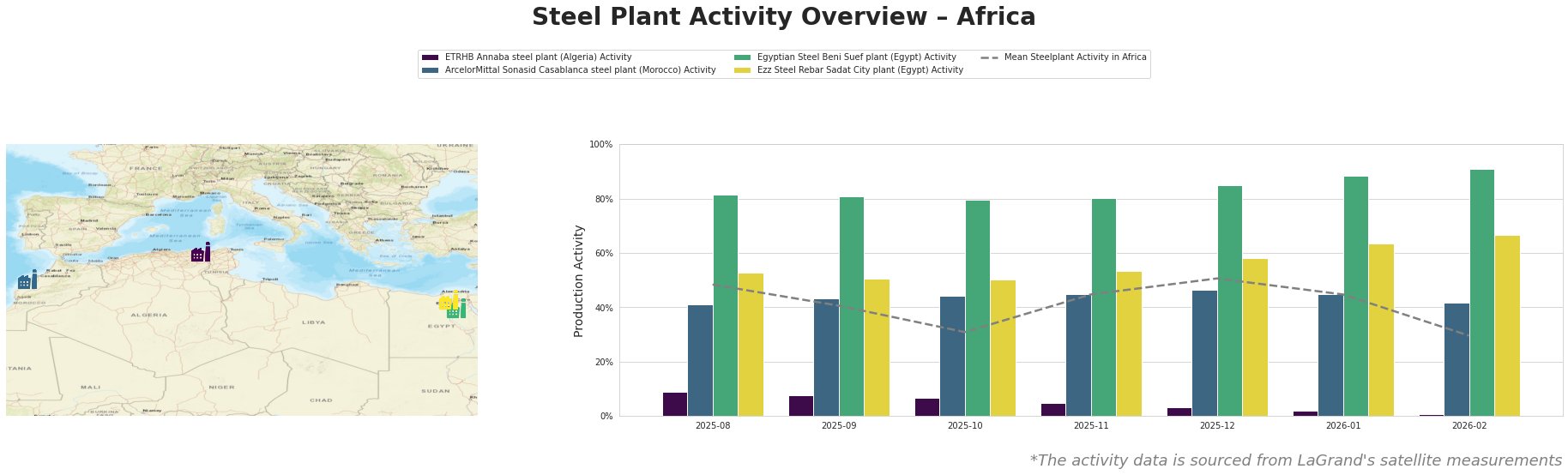

Recent activity data reveals a marked decline in performance across all observed plants; notably, ETRHB Annaba’s activity plummeted to 1.0% by February 2026, significantly below the mean of 30.0%. In comparison, although Egyptian Steel’s Beni Suef plant shows stronger performance, maintaining 91.0%, it reflects weak overall health in the sector. The drastic reduction at ETRHB Annaba may not have direct ties to the Simandou incident, but broader market sentiment is certainly affected by similar operational troubles as highlighted by Rio Tinto pauses Simandou iron ore mine in Guinea.

The ETRHB Annaba steel plant has experienced a decline in activity from 9.0% in August 2025 to a mere 1.0% by February 2026, amid safety and operational concerns, though no direct news link can be established for its closure. The plant primarily uses Electric Arc Furnace (EAF) technology to produce finished rolled products, yet the drop signals serious issues potentially hindering its competitive position.

The ArcelorMittal Sonasid Casablanca steel plant has also shown a slight decline from a stable operation of 45.0% in late 2025 to 42.0% in early 2026, indicating pressure from regional dynamics but lacking direct linkage to the iron ore supply disruptions at Simandou. This facility employs EAF technology, producing both semi-finished and finished rolled products vital for construction and infrastructure.

Conversely, the Egyptian Steel Beni Suef plant has seen relatively stable operations, with activity peaking at 91.0% in February 2026, driven by its important role in providing critical products like billets and rebar, although it remains impacted by the broader industry disruptions.

At the Ezz Steel Rebar Sadat City plant, activity also increased to 67.0% in the recent evaluation, suggesting adaptability to market demands, but still reflecting deeper issues in steel supply linked to iron ore availability.

Steel buyers should consider potential supply disruptions stemming from reduced output capabilities, particularly from plants like ETRHB Annaba, where operational viability has waned significantly. Strategic procurement should focus on sourcing materials from more stable facilities like Beni Suef, while keeping a close watch on iron ore supply implications from Guinea’s Simandou, as these factors continue to impact price and availability in the broader market.