From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEuropean Steel Market Report: Activity Surge Amid Positive Political Changes

In Europe, the steel market sentiment is notably Very Positive, driven by significant political developments and improved operational activity across key facilities. The articles “European carbon prices slide as Germany’s Merz says EU ETS may need revamping” and “European leaders seek ETS review amid energy concerns” emphasize a reevaluation of the EU’s Emissions Trading System, potentially fostering a more competitive pricing environment for steel producers. These discussions relate directly to increasing activity levels observed in steel plants, hinting at a resurgence in production capabilities.

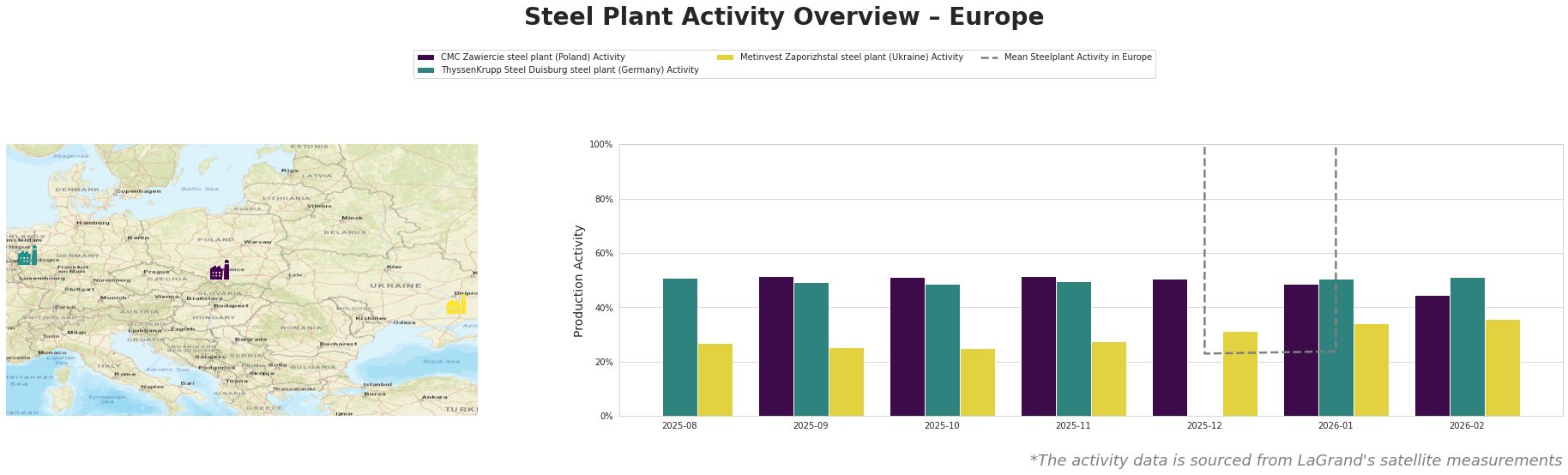

The CMC Zawiercie steel plant exhibits a stable trend near the average activity level, ranging from 49% to 52% recently. Operational resilience appears linked to potential reforms in the EU ETS, as discussed in the article “European carbon prices slide as Germany’s Merz says EU ETS may need revamping,” which suggests that policy adjustments could reduce competitive pressures and stabilize power costs.

The ThyssenKrupp Steel Duisburg plant, operating at 51% activity in the latest reporting month, reflects strong performance within the integrated steelworks sector. This aligns with political dialogues advocating for regulatory simplification, as reported in “European leaders seek ETS review amid energy concerns.” A stable operating environment helps safeguard this facility against fluctuation in raw material costs.

Conversely, the Metinvest Zaporizhstal steel plant shows increased variability, with activity levels bouncing from 25% to 36%. The engagement of political leaders in addressing carbon regulations may influence this plant’s future output, ensuring it can better align with European competitiveness goals emphasised during recent summits.

Observing these plants’ activities indicates an opportunity for strategic procurement ahead of anticipated market dynamism prompted by policy revisions. As market conditions evolve, it is advisable for steel buyers to evaluate supplier capabilities and establish sourcing agreements that account for potential fluctuations in availability tied to regulatory shifts.

Procurement Recommendations:

- Consider securing contracts with ThyssenKrupp, which displays consistent activity levels, as reforms may bolster their pricing competitiveness.

- Monitor CMC Zawiercie’s activities closely to assess how forthcoming changes in the EU ETS influence costs and output, thus informing future sourcing strategies.

- Prepare for potential supply variability from Metinvest Zaporizhstal, and consider establishing contingency plans to mitigate impacts from operational disruptions as the political landscape shifts.

These actions are crucial for maintaining a robust procurement strategy in the evolving European steel market.