From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEurope Steel Market: German Subsidies Threaten Czech Competitiveness Amidst Stable Plant Activity

Europe’s steel market faces potential disruptions due to uneven energy subsidies. As highlighted in “German power cap disadvantages Czechia, unbalances EU“, Germany’s electricity price cap gives its steelmakers a competitive edge over Czech producers. This issue is further compounded by the concerns raised in “Czech steelmakers concerned about German industrial electricity prices” and “The capacity restriction in Germany puts the Czech Republic at a disadvantage and upsets the balance in the EU“. While plant activity remains relatively stable, the long-term impact of these subsidies warrants close monitoring.

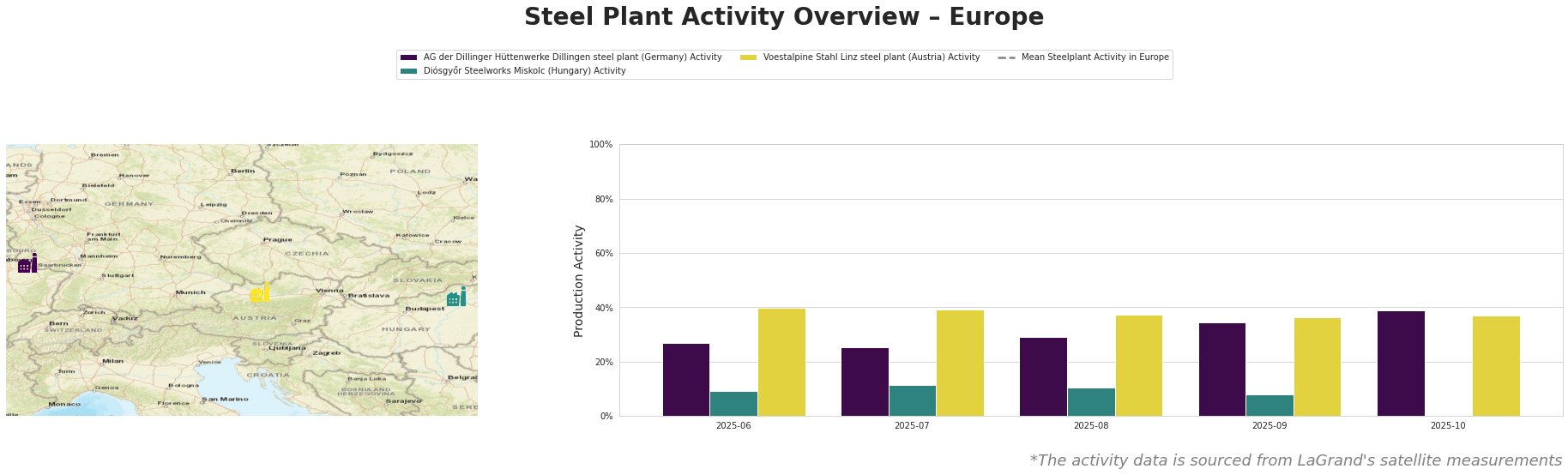

Across Europe, the mean steel plant activity fluctuated, peaking in July and August 2025 before declining through October.

AG der Dillinger Hüttenwerke Dillingen steel plant (Germany), an integrated BF/BOF steel plant in Saarland with a crude steel capacity of 2.76 million tonnes, saw activity increase from 27% in June to 39% in October. This increase potentially reflects the benefits of the electricity price support discussed in “Germany Commits to Steel Sector Competitiveness Through Electricity Price Support and Carbon Border Advocacy“, though a direct link cannot be definitively established. Dillinger’s focus on high-grade plate steel for industries like energy and infrastructure positions it to benefit from subsidized energy costs, enhancing its competitiveness.

Diósgyőr Steelworks Miskolc (Hungary), an EAF-based plant with a 0.55 million tonne capacity, showed fluctuating activity. It rose from 9% in June to 12% in July, then declined to 8% in September, with no data available for October. Given the focus of the news articles on Germany and the Czech Republic, no direct connection can be established between the plant’s activity and the reported developments.

Voestalpine Stahl Linz steel plant (Austria), a major integrated BF/BOF producer with 6 million tonnes of crude steel capacity, saw relatively stable activity between 36% and 40% from June to October. As with Diósgyőr, no direct connection can be established between the plant’s activity and the reported developments, as the news focuses on the Czech Republic and Germany.

The subsidized electricity prices in Germany, as reported in “Czech steel sector urges government action as Germany introduces subsidized electricity tariff“, create a competitive disadvantage for Czech steelmakers like Trinecke zelezarny, potentially impacting their production levels and market share.

Evaluated Market Implications:

The primary risk lies in potential supply disruptions from Czech steelmakers due to increased costs and decreased competitiveness caused by the German electricity subsidies. This could particularly affect buyers relying on specific steel grades or products sourced from the Czech Republic.

Recommended Procurement Actions:

- Diversify Sourcing: Steel buyers should evaluate alternative steel suppliers, particularly outside the Czech Republic, to mitigate potential supply disruptions. Focus on suppliers within the EU but outside of Germany, to avoid similar pricing disadvantages, or explore reliable international sources.

- Monitor Czech Steel Production: Closely track the production and financial performance of Czech steelmakers, such as Trinecke zelezarny, to anticipate potential output reductions or closures. This requires active communication with suppliers and monitoring of industry news specific to Czech producers.

- Negotiate Contracts: When negotiating contracts with Czech suppliers, understand their cost structures and potential challenges related to energy prices. Explore options for price adjustment mechanisms or flexible delivery schedules to accommodate potential disruptions.

- Assess German Steel Availability: Evaluate the potential for sourcing steel from German producers, considering that their competitiveness may increase due to the subsidies. However, be mindful of potential capacity constraints or lead time increases as demand shifts towards German suppliers.

- Advocate for Fair Competition: Support industry associations and government efforts to address the uneven playing field created by national-level subsidies. Advocate for EU-wide solutions that ensure fair competition and prevent market distortions.