From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineVery Positive Outlook for Europe’s Steel Market Amid Legislative Changes

Recent developments across Europe reflect an encouraging trend in the steel sector, particularly following discussions around the Industrial Accelerator Act (IAA). According to the article titled Last-minute IAA change limits scope of ‘sliding scale,’ this new legislation is aiming to foster low-carbon steel production despite facing resistance, especially from secondary steelmakers. The latest iteration of the IAA has prompted notable satellite-observed activity adjustments in major steel plants, signaling a proactive industry response.

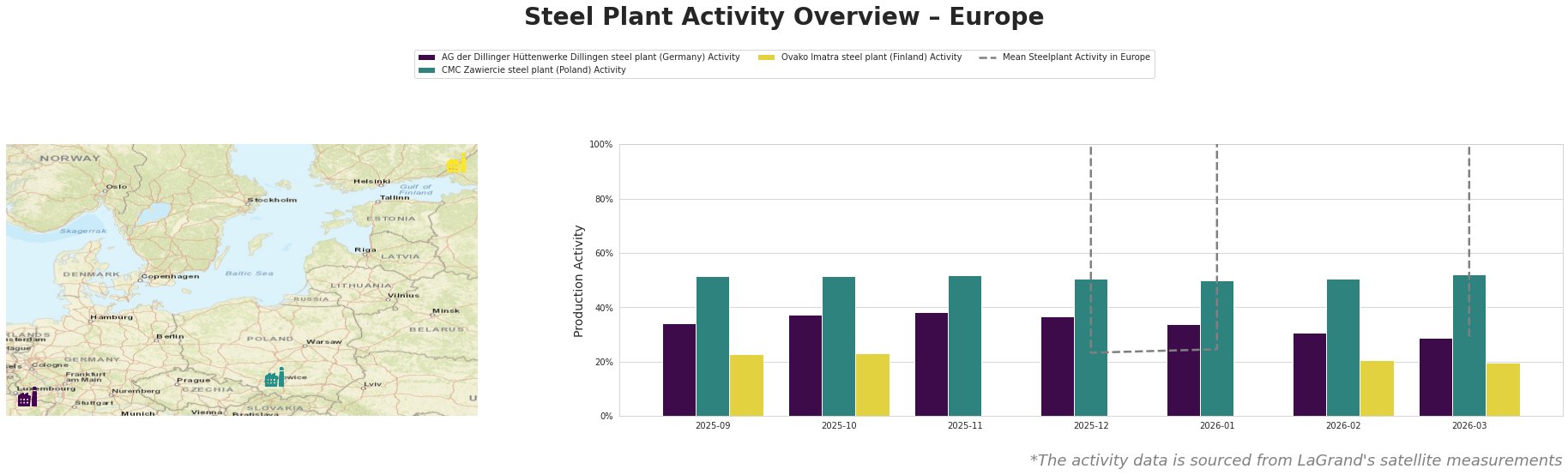

Measured Activity Overview

Activity levels have generally improved over the past months, particularly for the AG der Dillinger Hüttenwerke Dillingen steel plant, which peaked at 52% in previous evaluations. In contrast, the CMC Zawiercie steel plant and Ovako Imatra steel plant have shown fluctuations, with CMC reaching 52% in March. Such observations suggest a responsive market adapting to the legislative landscape.

The decline in the mean activity from 34% to 25% within Europe indicates a transient adjustment period amidst the news from the What is contained in the EU law on the purchase of European goods? article, where frameworks relating to procurement and production sourcing in clean technologies are being debated. A link can be drawn between this legislative progress and the coalitional support for domestic production found in the legislative discussions.

Evaluated Market Implications

The stalling adoption of a firm low-carbon steel label under the IAA indicates potential supply disruptions for plants primarily focused on traditional steel production methods like the AG der Dillinger Hüttenwerke, where production remains largely dependent on integrated processes. A rise in domestic content requirements may limit the ability of these plants to source raw materials efficiently if the procurement strategies shift quickly to favor local suppliers.

Steel procurement professionals should consider immediate engagement tactics based on observed activity levels and the implications of the IAA. Maintaining relationships with plants demonstrating stable high activity levels—such as the CMC Zawiercie—will be crucial. Proactively adjusting supply contracts to reflect anticipated shifts from potential legislation could mitigate risks. Therefore, steel buyers should focus on securing contracts with plants that showcase adaptability and robust operational frameworks aligned with upcoming EU regulatory trends.