From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineUkraine Steel Market: Activity Trends and Procurement Insights Amid Global Dynamics

Recent developments in Ukraine’s steel market reflect fluctuating plant activity levels, amidst evolving global trade dynamics. Notable news, such as the UK to remove Turkish HDG quota exemption and UK’s TRA amends TRQ for merchant bars, sections, suggest an impending pressure on supply chains influenced by international tariffs. No direct link, however, can be established between specific articles and plant activity changes.

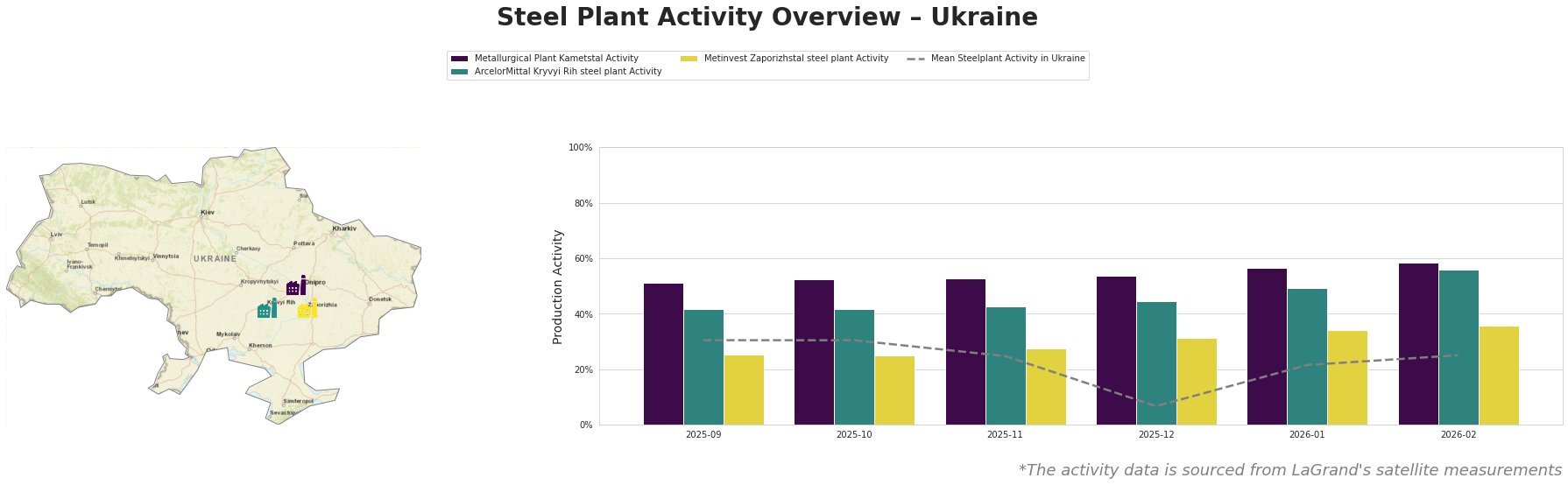

Measured Activity Overview

Recent data indicates a notable decline in overall activity, reaching a low of 7% in December 2025, rebounding to 25% by February 2026. The Metallurgical Plant Kametstal consistently outperformed others, peaking at 58% in February while the Metinvest Zaporizhstal plant showed only a modest recovery to 36%. However, the fluctuations do not seem to directly correlate with tariff changes reported in the news articles.

Plant Insights

Metallurgical Plant Kametstal in Dnipropetrovsk focuses on integrated processes using blast furnaces and basic oxygen furnaces. Its activity rose steadily from 54% in December to 58% in February 2026, potentially signaling increased demand for semi-finished products like billets. The demand shift could derive from broader market reactions to tariff reforms mentioned in UK’s TRA amends TRQ for merchant bars, sections, although no specific causal relationships can be confirmed.

ArcelorMittal Kryvyi Rih, one of Ukraine’s largest steel producers, experienced a rise from 45% in December to 56% by February. This plant specializes in a diverse range of products including rebar and merchant bars. The recent increase might indicate preparations for the anticipated changes in UK market requirements highlighted by the UK to remove Turkish HDG quota exemption news, which could elevate domestic steel production needs in the region.

Metinvest Zaporizhstal faced less significant surges, climbing from 31% to 36% in the same period, primarily producing hot-rolled coils and sheets. This gradual increase may reflect stable internal market demand, potentially insulated from external tariff pressures but demonstrates that production capacities remain underutilized.

Evaluated Market Implications

Given the upcoming modifications in UK trade policy, specifically the UK to remove Turkish HDG quota exemption, steel procurement professionals should brace for potential supply disruptions in Turkish steel imports. Ukrainian mills, notably Kametstal and Kryvyi Rih, may offer viable alternatives for sourcing amid escalating tariff complexities. Prioritizing relationships with robust domestic suppliers who can scale output in response to changing international dynamics is prudent.

Moreover, given that both Kametstal and Kryvyi Rih show resilience through their recent activity upticks, buyers may consider securing contracts with these firms to mitigate risks associated with external supply uncertainties. Continued observation of EU market protection measures, mentioned in The forecast for steel prices in the UK is strengthening due to the reform of protective measures and the change in the CBAM market, will further inform procurement strategies as markets evolve.