From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineSteel Market Report: Europe Sees Surge as ADI Increases Production Capacity

Acciaierie d’Italia’s (ADI) strategic moves in Italy, notably the Acciaierie d’Italia restarts BF No. 2 and Confectionery “Italy” reopens BF No. 2, have driven a significant shift in the European steel market. The reopening of BF No. 2 is set to double ADI’s steel production to 4 million tonnes per year by April 2026, coinciding with rising domestic prices fueled by the Carbon Border Adjustment Mechanism (CBAM) effects and reduced import quotas expected later in the year.

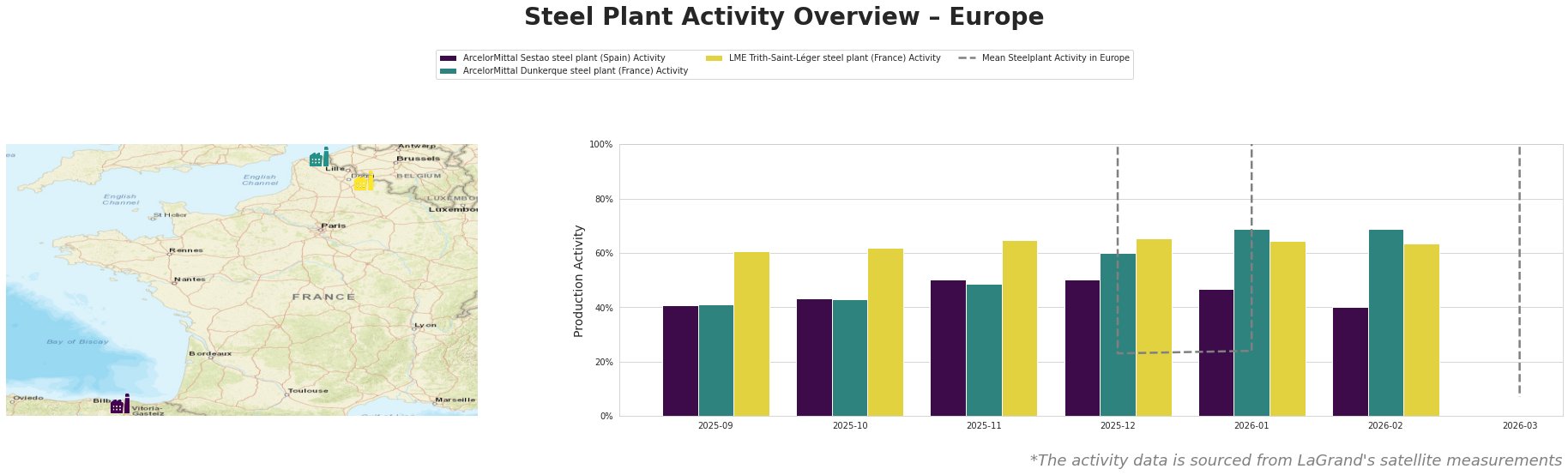

Recent activity trends show fluctuating production levels across key European plants. Notably, the ArcelorMittal Dunkerque plant saw a performance drop in January to 69%, a recovery to 69% again in February, directly aligning with ADI’s increased production activity as highlighted by the news articles concerning the restart of BF No. 2. The ArcelorMittal Sestao registered steady levels around 41% and 43%, closely tracking mean activity levels, while LME Trith-Saint-Léger peaked at 66% in December but showed diminished performance as observed in January and February.

ArcelorMittal Sestao, located in Biscay, utilizes Electric Arc Furnace (EAF) technology with a capacity of 2 million tonnes focusing on hot-rolled coil production. Its activity level remained stable but slightly below the mean, with recent operations not directly linked to the ADI news developments. In contrast, ArcelorMittal Dunkerque, with a higher capacity of 6,750 tonnes via integrated BF method, aligns its fluctuations to market demands influenced by ADI’s operational changes. Finally, LME Trith-Saint-Léger, operating entirely on EAF technology, peaked at 66% in December, but cannot be explicitly connected to the recent developments at ADI.

The growing domestic demand, driven by rising prices for hot-rolled coil at EUR 660-670/t, necessitates proactive procurement strategies. Steel buyers should prioritize sourcing from Italian producers like ADI, given the potential for increased domestic price stability amid declining imports due to the CBAM impacts. It is also advisable to monitor the maintenance schedule for BF No. 4 at ADI, which may lead to temporary supply constraints when it shuts down on February 28 for 60 days. This combined outlook suggests that buyers should strategically time their purchases, favoring early procurements to mitigate risks associated with potential supply disruptions.