From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineSteel Market Outlook for Asia: Activity Plummets Amidst Global Trade Uncertainty

The Asian steel industry is currently facing a very negative sentiment, primarily driven by significant geopolitical tensions, notably regarding the World Trade Organization (WTO). The articles “Welthandel unter Trump: Ist die WTO reformierbar?”, “Welthandel im Wandel – Die WTO muss reformiert werden, doch die Fronten sind verhärtet,” and “EU parliament approves US trade deal with strict safeguards” indicate that the ongoing difficulties faced by the WTO are adversely affecting trade policies and, consequently, steel demand in the region. Satellite-observed activity reveals sharp declines in operational levels at key plants, reflecting this bleak outlook.

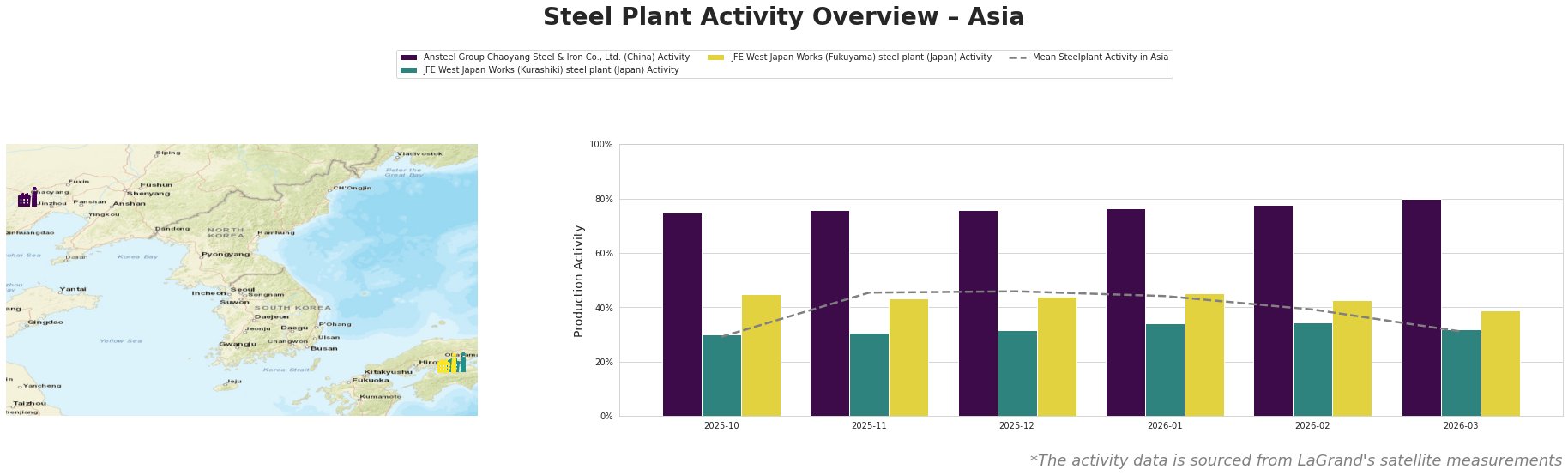

Activity levels at the Ansteel Group Chaoyang Steel & Iron Co., Ltd. have shown notable fluctuations, peaking at 80% in March 2026, prior to significant geopolitical trade constraints highlighted in the articles. This spike contradicts the overall market sentiment and is less aligned with recent drops in mean activity across Asia, which fell to 31% as of March. Both JFE West Japan Works plants reflect a contraction in output, with the Kurashiki plant recording a drop to 32% and the Fukuyama plant to 39%, continuing the downward trend noted since January 2026.

The Ansteel plant benefits from significant production capacity (Crude Steel: 2.1 million tons), primarily focusing on finished rolled products. The peculiar uptrend may stem from internal policy adaptations or targeted export contracts despite negative global sentiment. However, the diminishing overall activity signals potential supply vulnerabilities across the wider market.

Both JFE plants, integral to the automotive and construction sectors, reflected declining activity levels in line with reports on the WTO’s operational inefficiencies and challenges in maintaining trade flows amidst US tariffs. These declines reflect broader economic impacts discussed in “Welthandel im Wandel – Die WTO soll reformiert werden – doch wie ist umstritten”.

Potential supply disruptions are increasingly probable, especially from JFE’s facilities which, located in a more trade-reliant segment, are now exhibiting vulnerability to external trade policies. Consequently, steel buyers and analysts should initiate procurement actions focusing on diversifying supply sources, particularly favoring agreements with plants like Ansteel that demonstrated unexpected resilience. Prioritize purchasing in the short term while actively monitoring any shifts in geopolitical climates or further developments around the WTO to adapt procurement strategies accordingly.