From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineSteel Market Faces Downturn in Asia Amidst Middle East Tensions

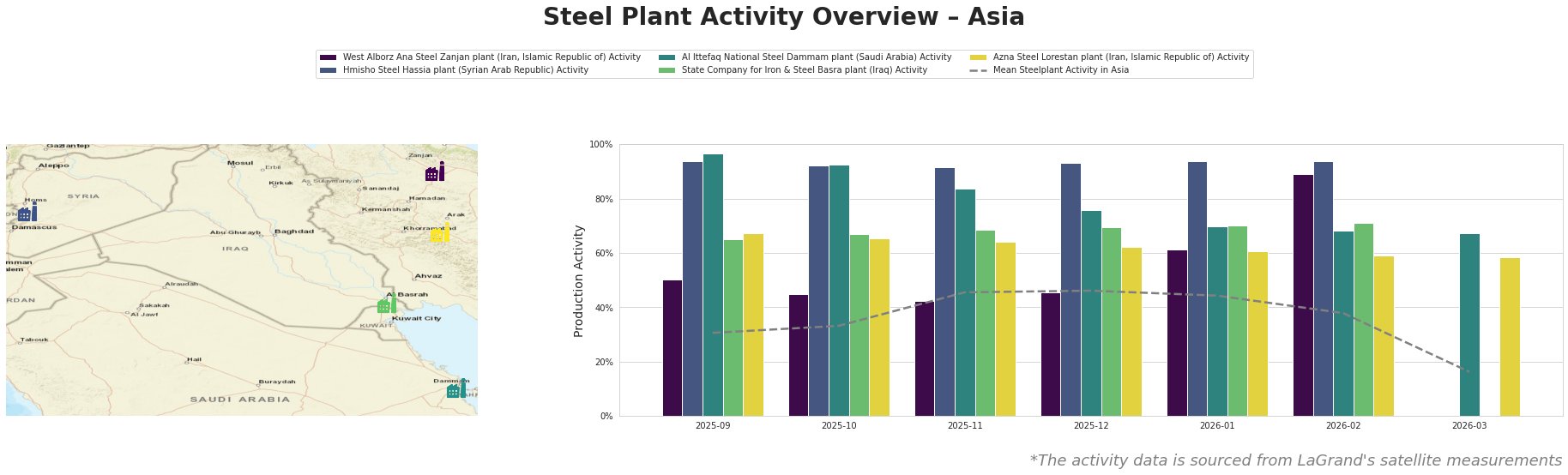

Recent geopolitical developments in the Middle East, particularly the escalating US-Iran conflict, are putting pressure on the Asian steel market. As per the article “Steel markets brace for Gulf conflict,” ongoing tensions threaten shipment routes, contributing to production cost increases and logistics challenges. Concurrently, observed satellite data indicates steep declines in activity levels at several Asian steel plants.

The West Alborz Ana Steel Zanjan plant witnessed a notable decline from 89% to 0% in activity by March, which could correlate with the increasing tensions highlighted in “Steel markets brace for Gulf conflict.” This drastic reduction in operational capacity raises concerns about supply consistency from Iranian steel suppliers.

The Hmisho Steel Hassia plant in Syria shows decreased consistent activity over the past months, reflecting broader regional instability, although direct links to specific geopolitical events aren’t established. The Al Ittefaq National Steel Dammam plant reported stable output until the recent month, maintaining its production levels close to full capacity since the conflict began, but could soon face disruptions if logistics issues escalate.

The State Company for Iron & Steel Basra and Azna Steel Lorestan plants’ operations have declined, dropping below 60% as of March 2026. This change may be indirectly influenced by supply chain disruptions due to tensions in the Gulf region, as noted in the news articles, although no direct connection can be established.

The overall activity across Asian steel plants plummeted from a mean of 38% in February to 16% in March, suggesting an immediate supply risk for buyers.

Recommendations for steel procurement:

– Prioritize sourcing from stable regions: Given the volatility in output from Iranian and Gulf region plants, buyers should seek alternative suppliers outside affected areas to prevent shortages.

– Monitor logistics costs closely: Increased shipping and insurance costs due to risk perception in Gulf shipping lanes may severely impact procurement strategies.

– Engage with suppliers for transparency: Ensure that suppliers provide regular updates on their operational statuses and potential disruptions to enhance planning.

Given the negative sentiment in the market, swift action may secure more favorable procurement terms before further disruptions arise.