From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EnginePositive Outlook for Europe’s Steel Market: Activity Surge and Tariff Adjustments

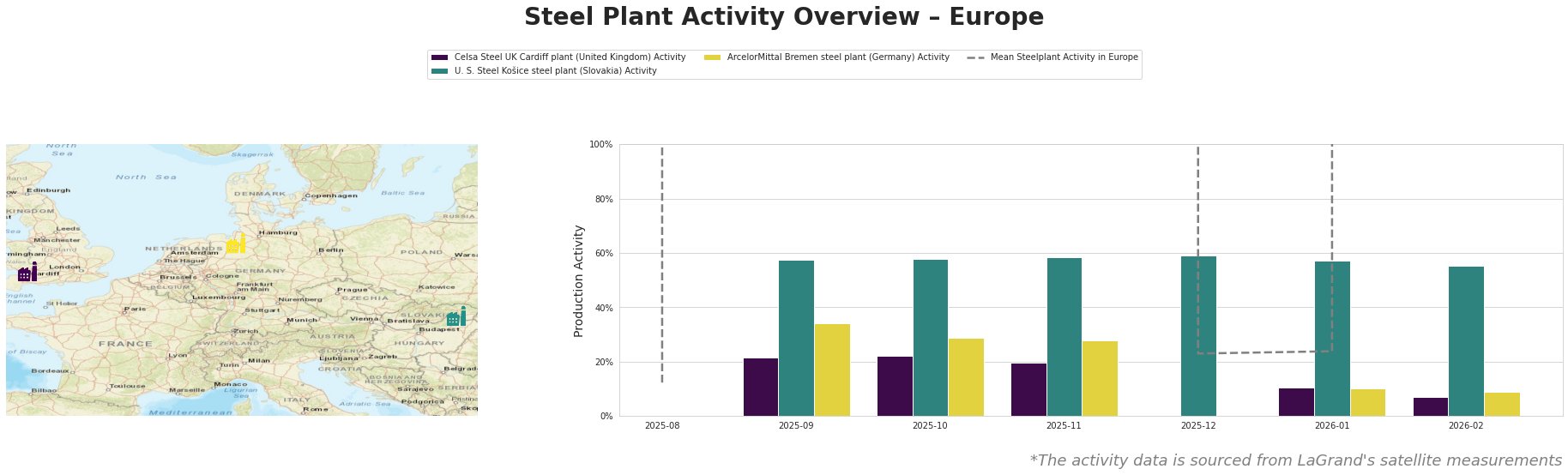

The European steel market is experiencing positive momentum, driven by significant tariff updates and increasing activity levels across key plants. Recent articles such as “UK’s TRA amends TRQ for merchant bars, sections“ and “TRA UK introduces changes to TRQ for shopping bars, sections“ highlight curbed domestic production and increased imports, which are reflected in observable plant activity shifts. Notably, the proposed adjustments by the UK’s Trade Remedy Authority (TRA) to focus on UK-produced goods are likely to enhance local production dynamics, though direct correlations with satellite data remain complex.

Celsa Steel UK Cardiff plant observed a notable drop to 7% activity in December 2025, which aligns with the “UK’s TRA amends TRQ for merchant bars, sections” article indicating the cessation of production of comparable goods by local competitors. The U.S. Steel Košice plant showcases resilience with activity peaking at 58%, following ongoing demand in automotive and construction sectors. ArcelorMittal Bremen, however, has faced relative declines recently, suggesting market adjustments in output strategies impacted by TRA decisions.

The U. S. Steel Košice steel plant, operating under an integrated (BF) process, reported a stable activity level in January at 57%, indicating steady demand despite competitive pressures from increased imports.

ArcelorMittal Bremen, focusing on finished rolled products, has seen decreasing activity levels, falling to 9% by late February 2026—a significant drop that underscores potential overcapacity concerns linked perhaps to the reported changes in import restrictions outlined in the UK TRA announcements.

Evaluated Market Implications

Disruptions may stem from fluctuating production capacities at the Celsa Steel UK Cardiff and ArcelorMittal Bremen plants, where recent drops have been evident. Given the TRA’s adjustment focus that favors local production yet does not revoke existing quotas entirely, buyers should anticipate potential volatility in domestic pricing structures and availability.

Procurement actions for steel buyers should focus on diversifying sourcing strategies, particularly towards Hungarian and Polish materials, as the UK shifts towards enhancing local outputs utilizing lighter tariff frameworks. Additionally, monitoring activity at the U. S. Steel Košice plant could yield competitive advantages in sourcing finished steel products, as its operations remain robust amid local challenges.

In summary, informed procurement based on the evolving landscape—especially considering the activity shifts and recent TRA announcements—will prove essential for effectively navigating the European steel market’s positive trend trajectory.