From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineOceania Steel Market Report: Neutral Sentiment Amidst Global Price Pressures

Recent developments in Oceania’s steel sector remain stable despite fluctuations observed elsewhere. Notably, the articles “European HRC prices continue to rise amid higher costs, limited availability and restricted imports“ and “European domestic steel HRC prices steady amid import limitations, low consumption“ highlight pressures from global markets affecting local dynamics. While these stresses are identified in Europe, no direct correlation can be firmly established with changes in local plant activity.

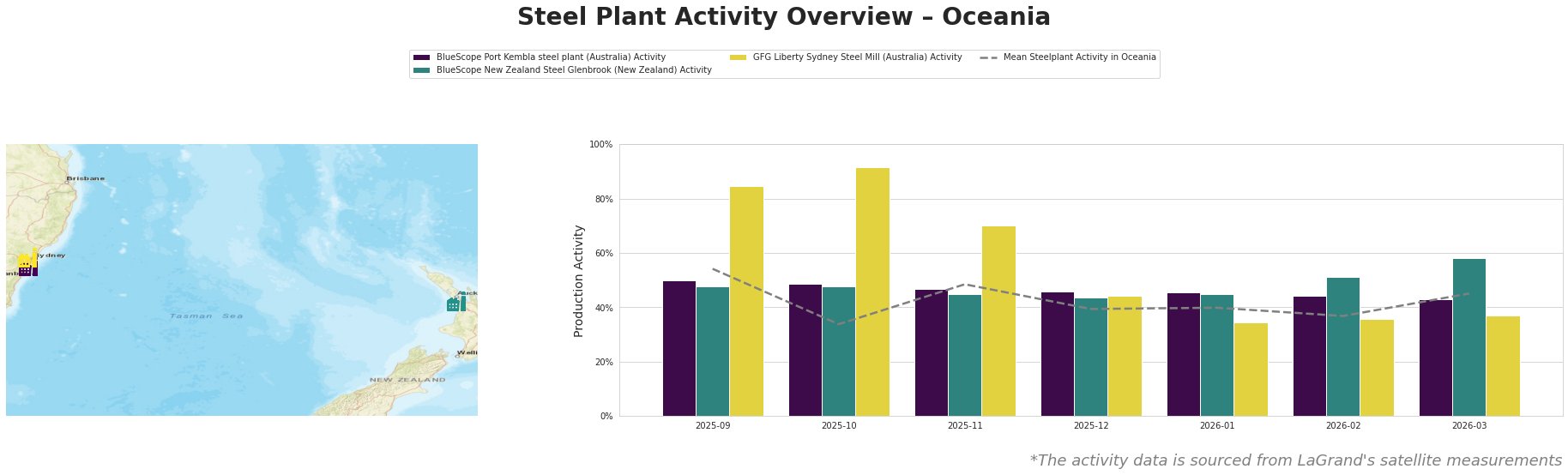

Overall, the mean activity across the observed plants displayed a notable decline in activity to 34% in October 2025, stressing the instability in local production. The GFG Liberty Sydney Steel Mill saw a constrained output decrease to 35% in January 2026 from a robust 92% in October 2025. BlueScope Port Kembla and Glenbrook have demonstrated more gradual fluctuations yet consistently remained below their earlier activity levels.

BlueScope Port Kembla, operating at a capacity of 3,200kt and focusing on finished rolled products, experienced a perturbed activity drop to 43% in March 2026 from 50% in September, amid elevated global slab prices reported in “European steel plate prices increase on higher slab and energy costs.” The plant’s output aligns with European pricing trends affecting local buyer sentiment.

BlueScope New Zealand Steel Glenbrook, with a DRI integrated process, registered a rise to 58% activity in March 2026 after a peak at 51% in February. This gradual growth may suggest responsiveness to demand fluxes amid limited availability in Europe; however, it is inconclusive whether this can be traced back to external pressures directly.

GFG Liberty Sydney Steel Mill faced back-to-back challenges as activity slipped further to 37% in March 2026, down from 85% in September 2025—indicating potentially significant supply disruptions that could affect buyers seeking timely deliveries of critical materials.

The overarching sentiment within the steel market remains neutral. However, the volatility in global pricing and potential import restrictions compel a reassessment of procurement strategies.

Recommended Actions for Steel Buyers:

1. Engage with Local Producers: Begin discussions with BlueScope Glenbrook due to its gradual recovery in output, signaling potential for improved delivery schedules in alignment with European trends.

2. Monitor GFG Liberty Activity: Maintain close observation on GFG Liberty’s output levels, given their rapid decline, which may prompt urgent stock-up strategies for critical steel products.

3. Consider Hedging Risks: Be prepared for possible fluctuations in pricing stemming from external factors, including geopolitical tensions impacting steel slab prices and importing costs in Europe.

These actions are essential to mitigate risks associated with procurement amid a neutral sentiment affected by global pressures and localized production adjustments.