From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineNegative Sentiment in Asia’s Steel Market Amid Geopolitical Tensions and Plant Activity Declines

Significant challenges are unfolding in the Asian steel market, exacerbated by geopolitical tensions that reflect diminished activity levels across key plants. Notable evidence can be drawn from the news article “European prices for HRC jumped due to fears of import disruptions,” which underscores the interconnection between imported steel supply and domestic market fluctuations. This corresponds to the observed drop in activity at several major plants, particularly reflecting the impact of redirected shipments and escalating energy costs.

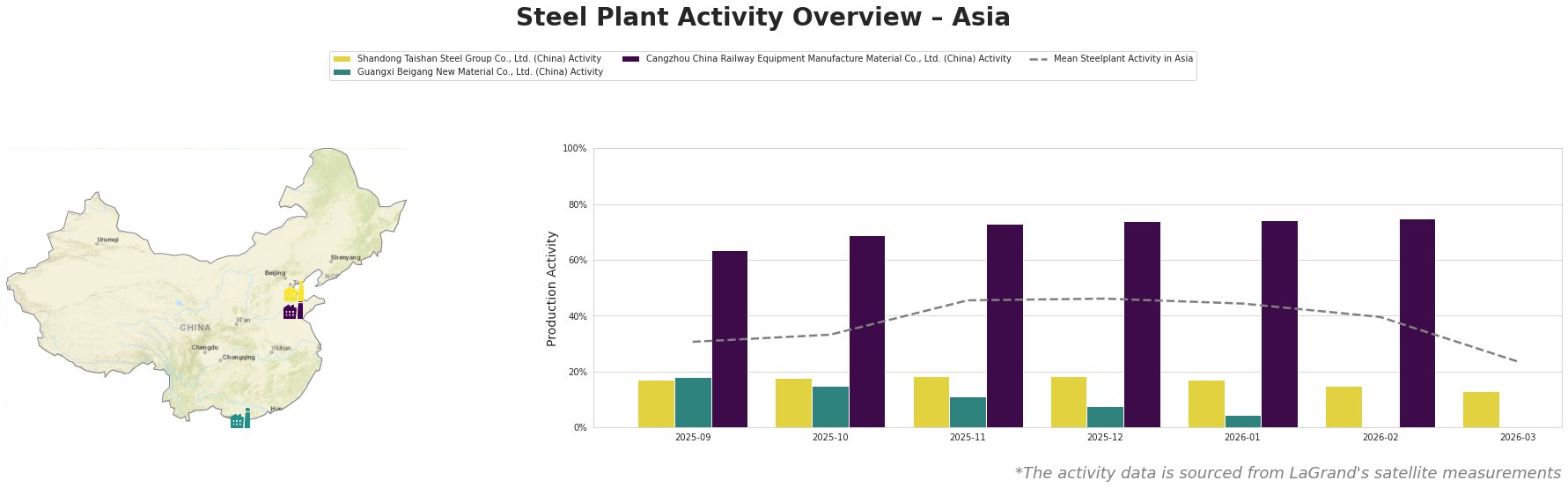

The activity of Shandong Taishan Steel Group has notably declined from 17% in September 2025 to just 13% in March 2026, reflecting a concerning downward trend that aligns with increasing pressures in the European market, highlighted in “Tight import supply, healthy order books help European HRC steel prices firm.” Despite a robust production capability of 5,000 tonnes crude steel per month, the plant’s recent activity is alarmingly low, which could threaten its competitive position amid tightening domestic and international supply scenarios.

Guangxi Beigang New Material also experienced a dramatic drop in activity, reaching 0% in February 2026. This aligns with concerns about supply disruptions referenced in “European coil and green steel round-up: EU coil prices hike on supply concerns as import risks compound,” suggesting that Asian producers are increasingly challenged by logistical issues that have historical parallels to crises like the COVID-19 pandemic.

Cangzhou China Railway’s activity remained relatively higher than other plants, at 75% in February but has seen stagnation signals that warrant close monitoring given the broader negative market sentiments in Asia.

The overarching implications for buyers are clear: there may be significant supply disruptions as both geopolitical tensions and logistical challenges exert pressure on steel production. Steel buyers should consider prioritizing procurement from plants with more stable operations like Cangzhou, while also preparing for potential price increases and longer lead times in light of the noted activity declines across multiple facilities. There is an evident urgency for proactive stockpiling strategies to mitigate against the anticipated supply volatility.