From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineInsights on Ukraine’s Steel Market: Activity Trends and Supply Chain Implications

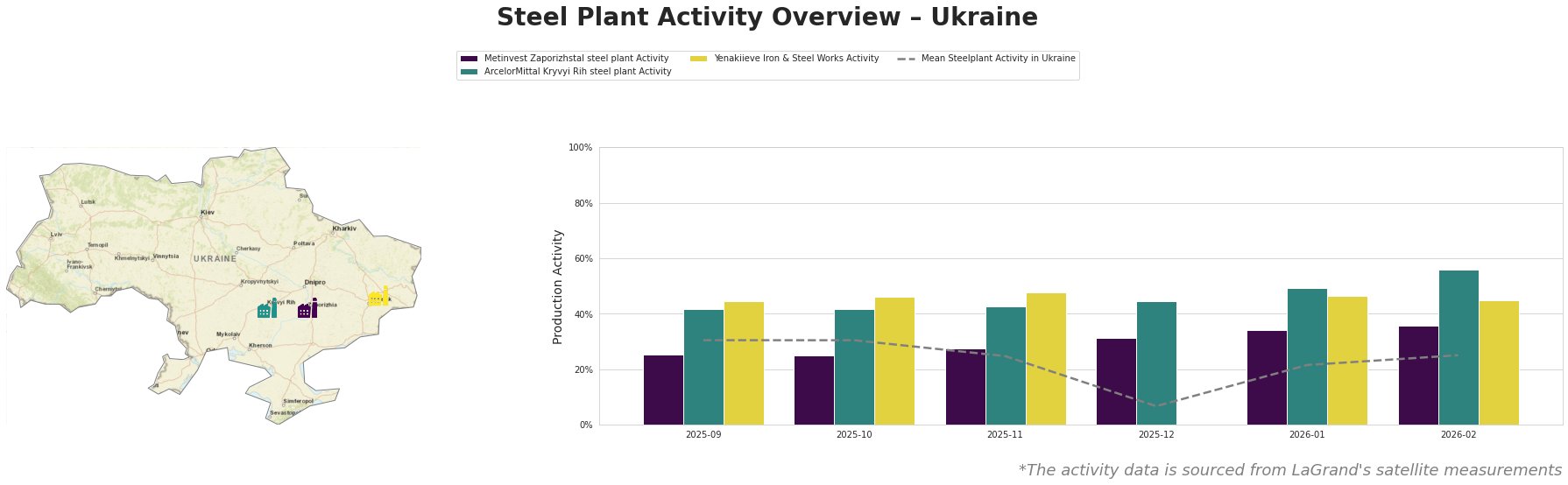

In Ukraine, significant changes in the steel market are emerging amidst ongoing geopolitical challenges. Recent news articles shed light on production and export dynamics: “Ukraine reduced its exports of long rolled steel by 62% y/y in January“ and “Ukraine increased ferroalloy production by 17% y/y in 2025.” These developments correspond to observed satellite data indicating steady but cautious activity levels across major steel plants.

The activity levels show a noteworthy fluctuation, with a significant drop to 7% in December 2025, indicative of potential operational disruptions, perhaps linked to the sharp decline in exports reported in January 2026. Metinvest Zaporizhstal and Yenakiieve Iron & Steel Works exhibit a recovery in early 2026, rising to 36% and returning to 45%, aligning with domestic shifts due to increased ferroalloy production as stated in “Ukraine increased ferroalloy production by 17% y/y in 2025.” ArcelorMittal Kryvyi Rih continues to lead in activity but must adapt to the decreasing export market.

At Metinvest Zaporizhstal, production capacity remains robust at 4,100 thousand tons of crude steel, focusing on finished products such as hot-rolled coils. Recent activity levels reflect a strategic pivot toward domestic consumption, influenced by increased local prices amid global market fragmentation. ArcelorMittal Kryvyi Rih, with an annual output capacity exceeding 8 million tons, has seen a surge in operational readiness; its January statistics suggest recovery post-export downturn. However, Yenakiieve Iron & Steel Works remains constrained, with operational capability at 3,300 thousand tons impacted by supply disruptions in its supply chain management.

Evaluated Market Implications:

Potential supply disruptions can be anticipated particularly for long rolled steel due to significantly diminished exports, specifically affecting Metinvest and ArcelorMittal’s operational outputs. Steel buyers should consider securing procurement contracts for semi-finished and finished products in advance, closely monitoring both domestic production capacities and market trends. Additionally, the stalled exports necessitate reevaluation of sourcing strategies, with an emphasis on negotiating favorable terms from local suppliers capable of adapting to changing demand dynamics and pricing structures. Always factor in the geopolitical landscape when assessing the long-term stability of supply chains in Ukraine’s steel sector.