From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEurope’s Steel Market Sees Positive Momentum as Domestic Supply Picks Up

European steel markets are experiencing a bullish shift due to notable domestic production increases amid rising import prices affected by the Carbon Border Adjustment Mechanism (CBAM). Key developments include Acciaierie d’Italia restarts BF No. 2 and Acciaierie d’Italia shuts down blast furnace No. 4 in Taranto for maintenance, which are linked to significant changes in production activities at several plants.

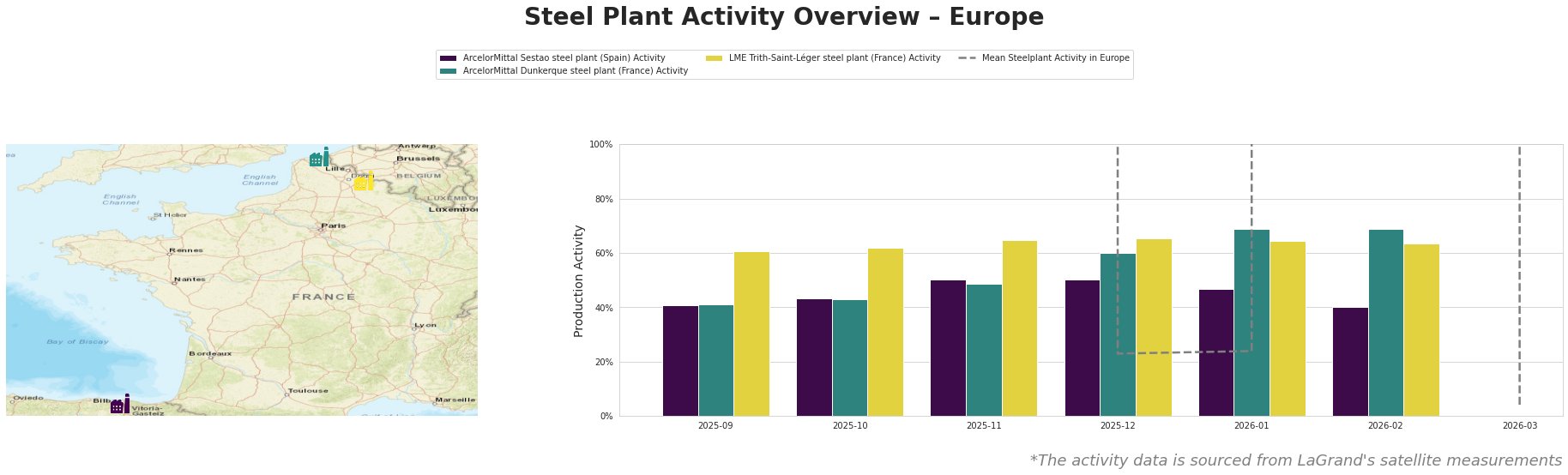

Recent satellite data indicates fluctuations in activity levels across various European steel plants, reflecting the market adjustments. Although the immediate connection to plant activity is inconsistent, the overall trend suggests a healthy shift toward domestic supply.

The ArcelorMittal Sestao steel plant recorded an activity level of 41% in September 2025, rising to 50% by November but retracting slightly to 40% in February 2026. This drop coincides with increased domestic competition for HRC following ADI’s restart of blast furnace No. 2, which is expected to bolster supply despite ongoing maintenance in Taranto.

The ArcelorMittal Dunkerque plant has been consistently strong, hitting 69% activity by January 2026, indicating stability in operations. This plant’s sustained output may be related to the uptick in domestic demand and growing interest from buyers shifting away from imports due to rising prices.

The LME Trith-Saint-Léger plant showed a high of 66% activity in December 2025, maintaining 64% through January and February 2026. This suggests that despite fluctuations, this facility is strategically positioned to serve the recovering market.

Given the information from the articles and data, it’s clear that European steel plants are adjusting operations in response to market dynamics favoring domestic production. Steel buyers should consider securing contracts with suppliers like Acciaierie d’Italia and ArcelorMittal Dunkerque, given their ramped-up production capabilities. Additionally, monitoring ongoing developments related to maintenance at ADI could provide insights into potential supply disruptions or shifts in pricing as the market evolves.

For procurement professionals, diversifying sourcing strategy to emphasize domestic supply from plants demonstrating resilience and higher activity levels may mitigate risks associated with rising import costs and ensure steady material flow into projects.