From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEurope’s Steel Market Faces Turmoil: Plant Activities Decline Amid Rising Compliance Costs

Europe’s steel market sentiment is notably negative, driven largely by the ramifications of the EU’s emissions policies and a concerning trend towards industrial desertification, as discussed in EUROMETAL Southern Europe Meeting 2026: The shadow of industrial desertification (2026-03-01). Furthermore, rising costs connected to the Carbon Border Adjustment Mechanism (CBAM) and emissions verification challenges have exacerbated plant activities, as outlined in Dutch parliament urges government talks with steel sector over CBAM cost issues (2026-03-06).

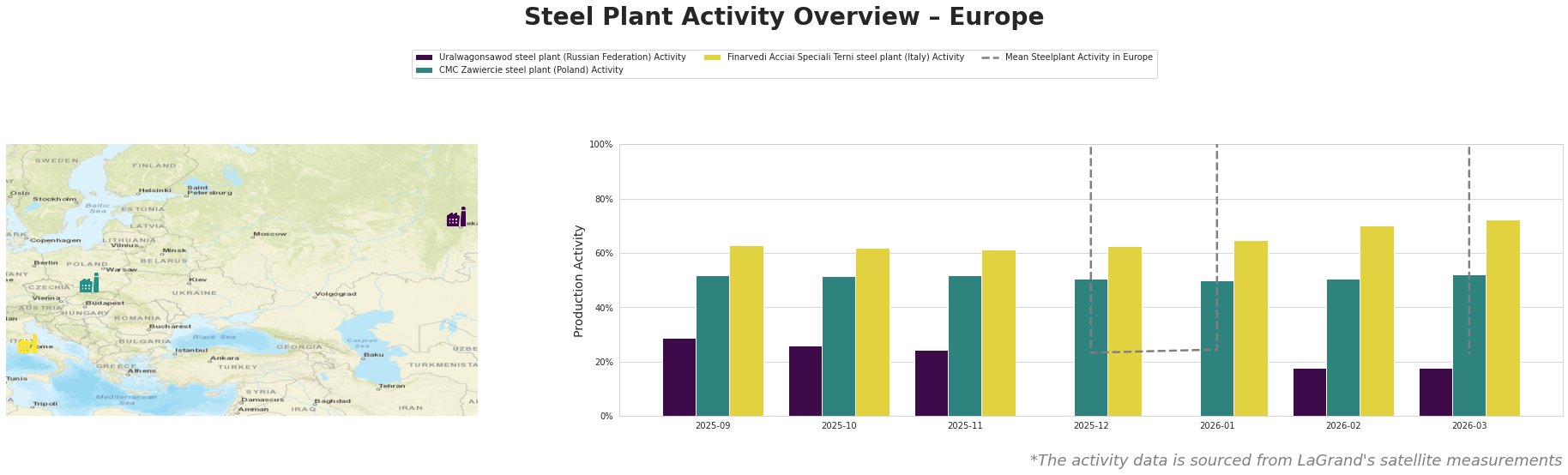

Recent satellite observations reveal a troubling decline in the activity levels of key steel plants across the region:

Activity levels in Europe have seen a severe drop, with a significant plunge observed in the Uralwagonsawod steel plant, which declined from 29% to 18% between February and March 2026. This aligns with the overarching narrative of reduced operational capacity discussed at the EUROMETAL meeting, alongside the challenges placed by climate regulations. CMC Zawiercie and Finarvedi, though less impacted relative to Uralwagonsawod, displayed only minor fluctuations, indicating a more stable but still concerning environment, corroborating calls from Italy, France push EU for faster ETS, CBAM reforms to protect industry (2026-03-05).

The activity at Finarvedi’s plant, while increasing slightly from 70% to 72%, may not suffice against the backdrop of increasing operational pressure. Furthermore, CMC Zawiercie’s stability at 52% juxtaposes the urgent industry needs emphasized in the aforementioned news articles. The interdependencies within these operational dynamics call attention to potential supply disruptions for critical products.

In summary, the significant decline in Uralwagonsawod’s performance points to the potential for severe supply disruptions in Eastern Europe, while stabilization efforts in Poland and Italy might lead to improved but still fragile production capabilities. Steel buyers and analysts should consider diversifying procurement strategies, particularly prioritizing suppliers with stable activity levels. Engaging in negotiations with domestic plants, particularly in Poland and Italy, can mitigate risks from volatility in Eastern supply chains, as emphasized by recent market dynamics and ongoing industry advocacy for reform in carbon pricing mechanisms.