From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEurope’s Steel Market Faces Downturn: Ukraine’s Production Struggles and Falling Activity Levels

Recent data reveals a troubling decline in the steel market across Europe, primarily influenced by production challenges in Ukraine. According to the article “Ukraine reduced rolled steel production by 18.2% y/y in February“, steel production in Ukraine faced a significant downturn, decreasing by 13.2% in January-February 2023 compared to the previous year. Furthermore, the article “Ukraine reduced iron ore exports by 40.9% y/y in January-February“ highlights that export constraints from Ukraine, stemming from power disruptions related to ongoing conflicts, have further exacerbated the regional supply landscape.

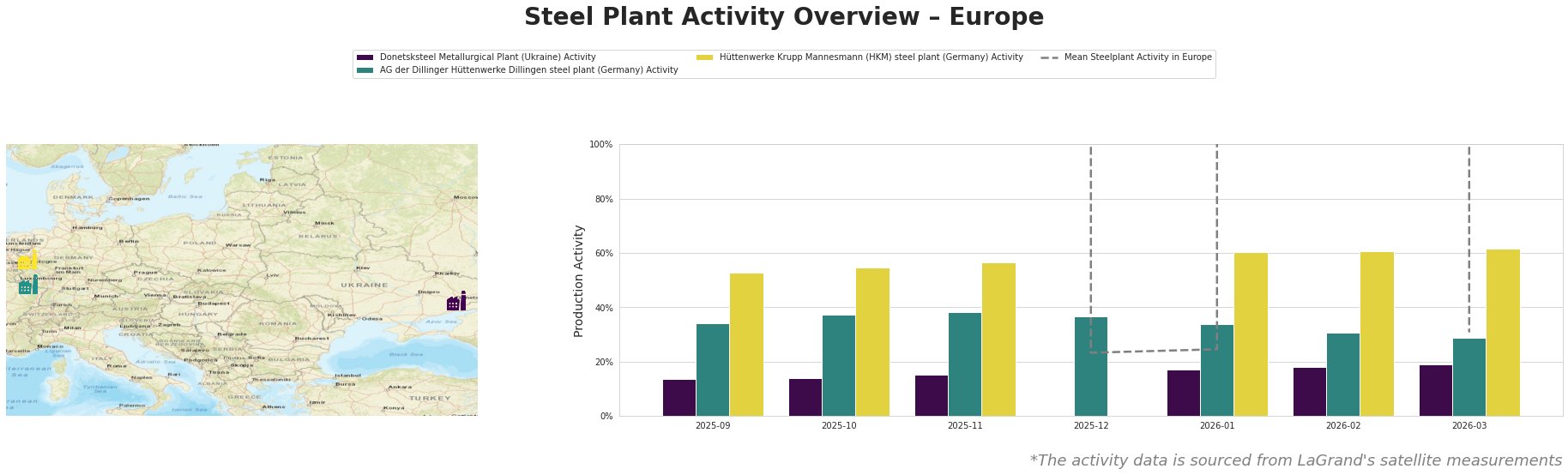

The observed satellite data underscores the negative trend; the mean activity across European steel plants dropped markedly, signaling overall industry distress. For example, the Donetsksteel Metallurgical Plant’s activity fell to 19% in March 2026, reflecting a 36.6% drop since September 2025, thus aligning with the production shortages discussed in the aforementioned articles.

At the Donetsksteel Metallurgical Plant, activity plummeted from 14% to 19% between September and March, mirroring Ukraine’s production reductions highlighted in the news. This plant, primarily producing pig iron, faces not only operational challenges but also diminished production capacity due to external conflicts.

AG der Dillinger Hüttenwerke maintained a relatively stable activity range, decreasing slightly to 29% by March 2026 but positioning itself as a critical supplier in a declining market. Meanwhile, Hüttenwerke Krupp Mannesmann (HKM) showed a minor increase to 62% in March, providing a slight buffer against the overall downturn.

The combined factors indicate potential supply disruptions, particularly evident in regions relying on Ukrainian steel, where production cuts threaten the stability of the supply chain.

For steel procurement professionals, immediate actions are recommended:

– Diversify Supply Chains: Given the ongoing production constraints in Ukraine, explore suppliers beyond the traditional Ukrainian sources to mitigate risks.

– Monitor Activity Levels Closely: Regularly assess the operational efficiency and activity levels of European steel plants to make informed procurement decisions, especially focusing on plants such as AG der Dillinger, which are less affected by current volatility.

– Evaluate Future Contracts: Given the projected decline in steel production as cited in the articles, negotiate contracts that provide flexibility in sourcing quantities as market conditions evolve.

In conclusion, the negative sentiment within the steel market necessitates strategic adjustments by buyers to navigate the impending supply challenges effectively.