From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineDisruptions Ahead as Iranian Steel Plants Face Air Strikes, Impacting Production and Trade in Asia

Recent tensions in the Middle East have severely impacted the steel industry in Asia, particularly in Iran. The “Iranian steel plants damaged by air strikes“ and “Iran is losing its steel production capacity due to the conflict in the Middle East“ articles outline the deterioration of operational capabilities at Khouzestan Steel (KhSC) and Mobarakeh Steel (MSC), stemming from recent air strikes. These attacks have caused significant damage to critical infrastructure, likely leading to production hesitations and potential shortages in the coming months, linking directly to declines in satellite-observed plant activity levels.

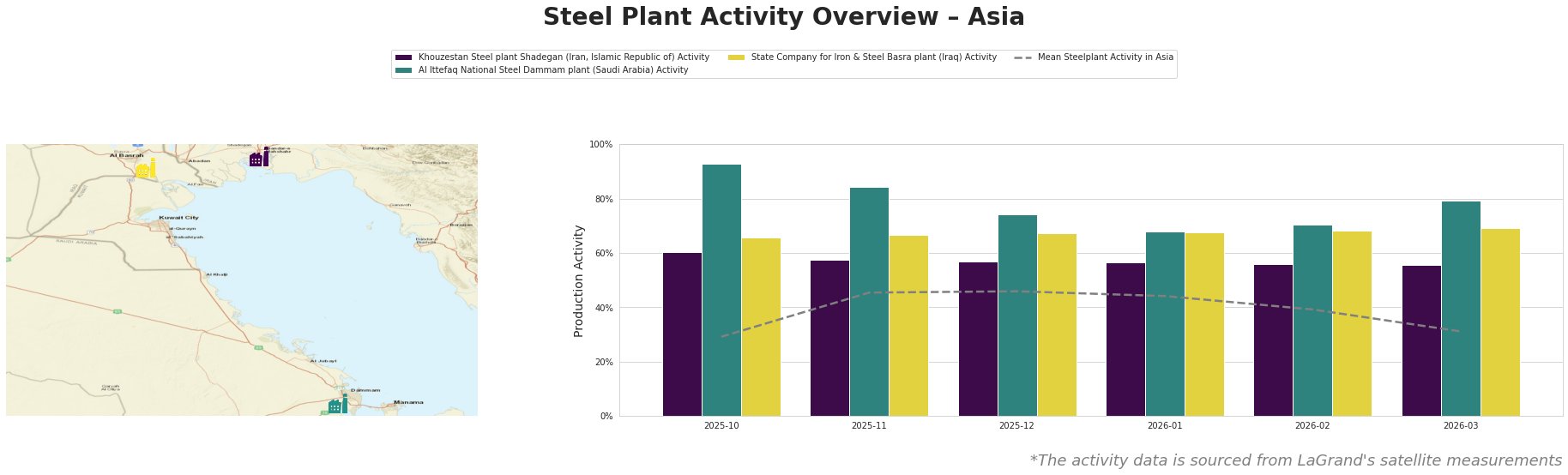

The Khouzestan Steel plant maintained an activity level of 56% as of March 31, 2026, reflecting a stable yet low performance, likely influenced by the “Iranian steel plants damaged by air strikes” report. This stability comes amidst damaged facilities but indicates limited immediate impact on the blast furnace operations. Production assessments, however, have not been finalized, suggesting further disruptions may follow. Al Ittefaq National Steel in Saudi Arabia shows relatively high activity levels but needs to prepare for potential price increases if Iranian supply diminishes. By contrast, the State Company for Iron & Steel in Iraq remains stable with 69% activity, likely insulated from Iranian disruptions.

Khouzestan Steel, with a capacity to produce 3.6 million tons of crude steel, focuses on semi-finished products. Its activity aligns with the recent strikes that damaged its storage silos, although direct losses remain unspecified. Al Ittefaq, capable of producing 1 million tons, has generally high activity levels indicative of robust demand but might face pressure due to Iranian market volatility. Basra’s operations are stable but will need to navigate a market that may tighten due to broader Iranian supply issues.

Steel buyers should prepare for potential supply disruptions, especially for semi-finished products like billets and slabs from Iran. Given the uncertainty surrounding the recovery of impacted plants and the possibility of retaliation disrupting further production, timely procurement actions are essential. Buyers should consider exploring alternatives or increasing stockpiles to hedge against anticipated price volatility and supply shortages. Engaging with suppliers of major semi-finished products, particularly outside of the impacted regions, may also mitigate risks tied to these developments.