From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineBrazilian Steel Market: Import Quota Utilization Rises Amidst Production Dip, Freight Rate Increase

Brazil’s steel market presents a mixed landscape, influenced by import dynamics and domestic production trends. As reported in “Brazil updates utilization of steel import quotas,” utilization reached 68% by mid-August, potentially impacting future import volumes and prices. The “Brazilian crude steel production declined in July 2025” article highlights a 9.6% year-over-year decrease in crude steel production, contrasting with the quota utilization. The rise in freight rates, detailed in “Freight rates increase slightly in July 2025 for Brazilian finished steel imports,” adds further complexity to the import landscape, especially from key suppliers like China. There is no explicitly established relationship between the production decline and the import quota utilization or freight rate increases based on the news articles.

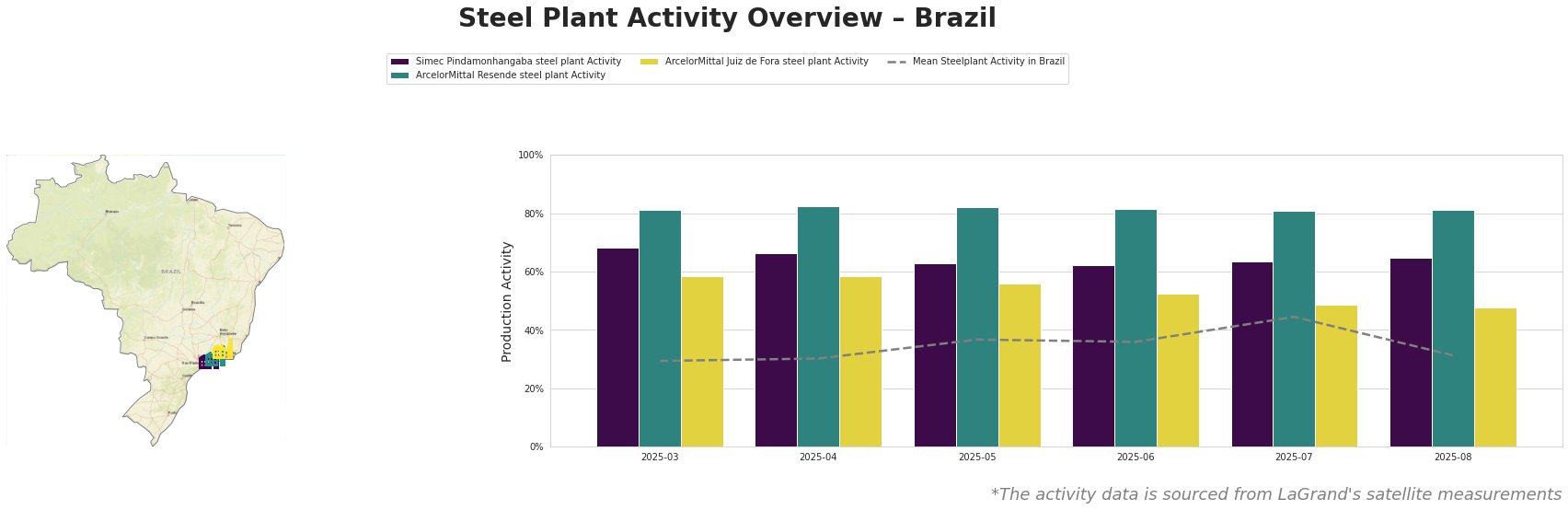

Monthly activity levels across selected steel plants in Brazil are as follows:

The mean steel plant activity in Brazil shows a peak in July (44%) before declining to 31% in August. Simec Pindamonhangaba maintains a relatively stable activity level, hovering between 62% and 68%. ArcelorMittal Resende shows the highest consistently high activity, ranging from 81% to 82%. ArcelorMittal Juiz de Fora activity declined steadily from 58% in March and April to 48% in August. These satellite-observed plant activities cannot be directly linked to the news articles about production and imports.

Simec Pindamonhangaba steel plant: This plant, located in São Paulo, has an EAF-based crude steel capacity of 500 ttpa and focuses on finished rolled products like wire rod and rebar for the building and infrastructure sectors. The plant’s activity remained relatively stable, ranging from 62% to 68% over the observed period. There’s no immediate correlation between this stable operational level and the reported decrease in national crude steel output or shifts in import quota utilization.

ArcelorMittal Resende steel plant: Situated in Rio de Janeiro, ArcelorMittal Resende possesses an EAF-based crude steel capacity of 1000 ttpa, also specializing in rebar and wire rod. It shows the highest activity level with consistently high activity, ranging from 81% to 82%. The stable activity does not directly reflect the crude steel production decline reported nationally.

ArcelorMittal Juiz de Fora steel plant: Located in Minas Gerais, this integrated plant combines BF and EAF processes with a crude steel capacity of 1100 ttpa and an iron capacity of 360 ttpa. The plant produces rebar, wire rod, and bars. The satellite data showed a steady decline in activity from 58% in March/April to 48% in August. This decrease in activity cannot be directly linked to the steel production decline but may contribute to it.

Evaluated Market Implications:

The increase in freight rates reported in “Freight rates increase slightly in July 2025 for Brazilian finished steel imports“, combined with high import quota utilization (“Brazil updates utilization of steel import quotas“) and decreasing domestic crude steel production (“Brazilian crude steel production declined in July 2025“) could create a supply squeeze, increasing the risk of potential price increases.

Given the 68% utilization of import quotas, especially for products like zinc coated (60%) and galvalume (69%), steel buyers should:

- Accelerate procurement: Secure necessary volumes promptly to avoid potential supply constraints as quotas fill.

- Diversify sourcing: Explore alternative suppliers, especially from countries with lower freight rates (e.g., South Korea and Egypt for HRC).

- Negotiate freight terms: Given rising freight costs, negotiate favorable terms with suppliers and consider alternative shipping arrangements.

For market analysts, the rising freight rates coupled with import quotas and declining production present opportunities to:

- Monitor quota utilization: Closely track the remaining quota volumes and anticipate potential policy adjustments by Siscomex.

- Analyze regional price variations: Investigate price differences across regions due to varying import costs and local production levels.

- Assess impact on end-user sectors: Evaluate how these market dynamics will affect the building and infrastructure sectors, key consumers of rebar and wire rod.