From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEurope Steel Market Report: Impacts of New Import Quotas and Activity Trends

The European steel market remains in a Neutral sentiment amid impending changes in import quotas. Recent articles such as “In Britain, warnings are being issued about the threat to business posed by new steel import quotas“ and “Tariff quota negotiations are politicizing European steel imports“ highlight significant concerns regarding the potential negative effects on steel procurement dynamics across the region as new import tariffs and quotas take effect on July 1, 2026. However, specific satellite observations do not establish a direct correlation between these changes and recent activity fluctuations at various steel plants.

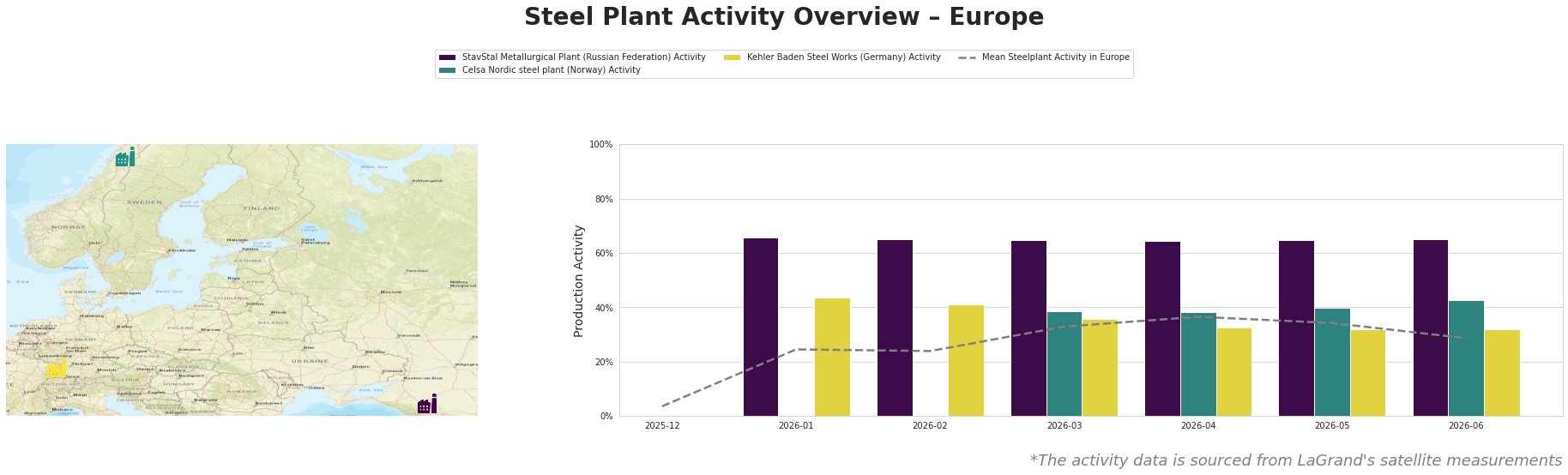

Activity levels across observed plants reflect notable constancy at the StavStal Metallurgical Plant, maintaining a consistent 65% utilization over the observed months, aligning with concerns stated in “BCC warns UK steel import restrictions could create ‘cliff-edge’ for manufacturers“. Despite the stable behavior, the average activity still hovers below the recent peak of 37% in April. Meanwhile, Kehler Baden Steel Works shows signs of slight contraction, dropping from 41% in February to 32% in June. The increase from 38% to 43% at Celsa Nordic indicates more robust activity in the face of these regulatory changes.

The StavStal Metallurgical Plant, located in Stavropol Krai, relies primarily on electric arc furnace (EAF) technology and has seen stable activity levels (65%) since January. This situation may reflect the relatively limited impact of new tariff discussions on domestic operations. Nevertheless, the climatic trade negotiations and proposed restrictions may pose latent risks to this steadfast productivity.

The Celsa Nordic steel plant in Mo i Rana has shown a slight uptick in activity from 40% to 43%. This resilience may suggest a strategic maneuvering to boost output before the anticipated tariff hikes, positioning the plant favorably to capture any immediate demand spikes despite the uncertainty in import quotas.

Kehler Baden Steel Works‘s decline from 41% in February to 32% by June implies a difficult landscape for meeting local demand amidst mounting import tariffs. This drop may relate to heightened operational costs as outlined in articles like “British steel fabricators are calling for the new steel measures to be revised,” where local fabricators express concerns over rising expenses driven by stricter tariffs impacting their supply chains.

The potential supply disruptions appear most relevant concerning Kehler Baden Steel Works, where decreased activity may further exacerbate supply challenges as availability of imported materials becomes strained post-regulation alteration.

Steel procurement professionals should closely monitor developments in tariff negotiations while reassessing sourcing strategies, with recommendations to:

- Prioritize sourcing from the Celsa Nordic steel plant, which has demonstrated increased resilience and output in current market conditions.

- Assess potential risks and delays in procurement with the upcoming changes, especially related to imports expected to face heightened tariffs and reduced quotas.

These tailored approaches aim to navigate the shifting landscape effectively while mitigating the risks stemming from the evolving regulatory environment in Europe’s steel sector.