From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineBrazil’s Steel Market Shows Positive Trends Amid Import Regulation Changes

Brazil’s steel industry has recently experienced notable shifts driven by regulatory measures and changes in plant operations. Key articles, such as “Brazil’s galvalume imports from China decline due to antidumping measures“ and “Brazil renews quota policy for import steel,” highlight the reductions in Chinese galvalume imports due to antidumping duties and an extension of steel import quotas, respectively. Notably, these regulatory actions have correlated with satellite-observed activity levels at Brazilian steel plants, indicating a positive market sentiment.

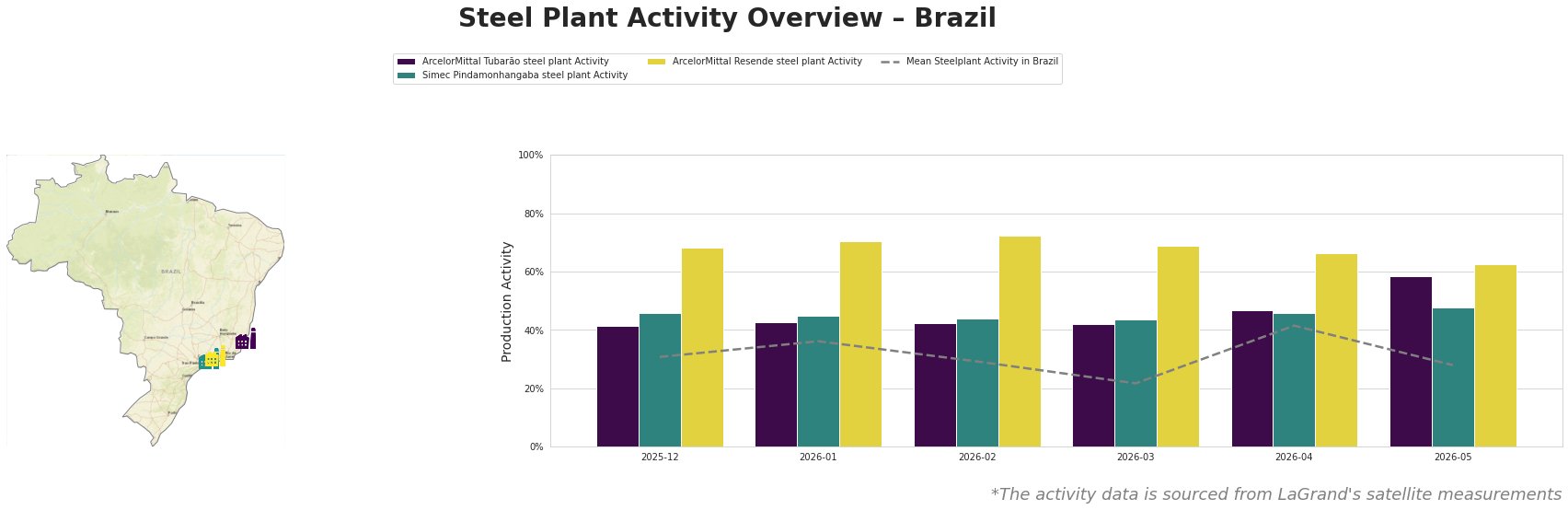

Recent activity data shows a general average steel plant activity increase to 42.0% in April from a dismal average of 22.0% in March, with dips noted in May (28.0%). Particularly noteworthy is ArcelorMittal Tubarão, which escalated its activity to 58.0% in May following a moderate 47.0% in April. This spike aligns with increases in import quota allocations for coated flat steel. Meanwhile, Simec Pindamonhangaba has maintained relative stability but demonstrates lower activity levels compared to its peers.

The ArcelorMittal Tubarão plant, located in Espírito Santo, operates with a capacity for 7,500 MT of crude steel using integrated production processes. The recent surge in activity level from 41.0% in December 2025 to 58.0% in May 2026 coincides with the news of reduced galvalume imports from China, providing space for increased domestic production. Meanwhile, at the Simec Pindamonhangaba plant, which focuses on electric arc furnace (EAF) production of finished rolled products, a consistent activity level of around 46.0% indicates stability despite ongoing quota measures mentioned in “Steel import quota utilization showing modest progress in Brazil.” This implies that while the plant is active, it is not expected to scale up substantially in the short term.

In light of current trends and upcoming regulatory frameworks, steel buyers and market analysts should be vigilant about the implications of continued export quotas. Given the evident decrease in foreign competition from China and a shift towards local producers—reflected in the increases in activity for Tubarão—it is advisable for purchasers to secure contracts with domestic steel suppliers ahead of potential supply disruptions, especially for coated flat products. Steel procurement professionals should also explore opportunities with plants like Simec Pindamonhangaba, which cater specifically to local demands in the infrastructure sector, albeit with caution given their lower activity levels.

Overall, the Brazilian steel market displays overall optimism, supported by local demand adjustments and regulatory changes aimed at stabilizing the industry amidst shifting global trade dynamics.