From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EnginePositive Momentum in China’s Steel Market: Satellite Data and News Insights

China’s steel industry demonstrates a positive outlook despite recent production declines. Notably, “China’s crude steel output down 3.5 percent in April 2026, maintaining downtrend in Jan-Apr” correlates with observed reductions in steel plant activity, while “Global steel production fell by 4.1% m/m in April” emphasizes a broader trend affecting global supply chains.

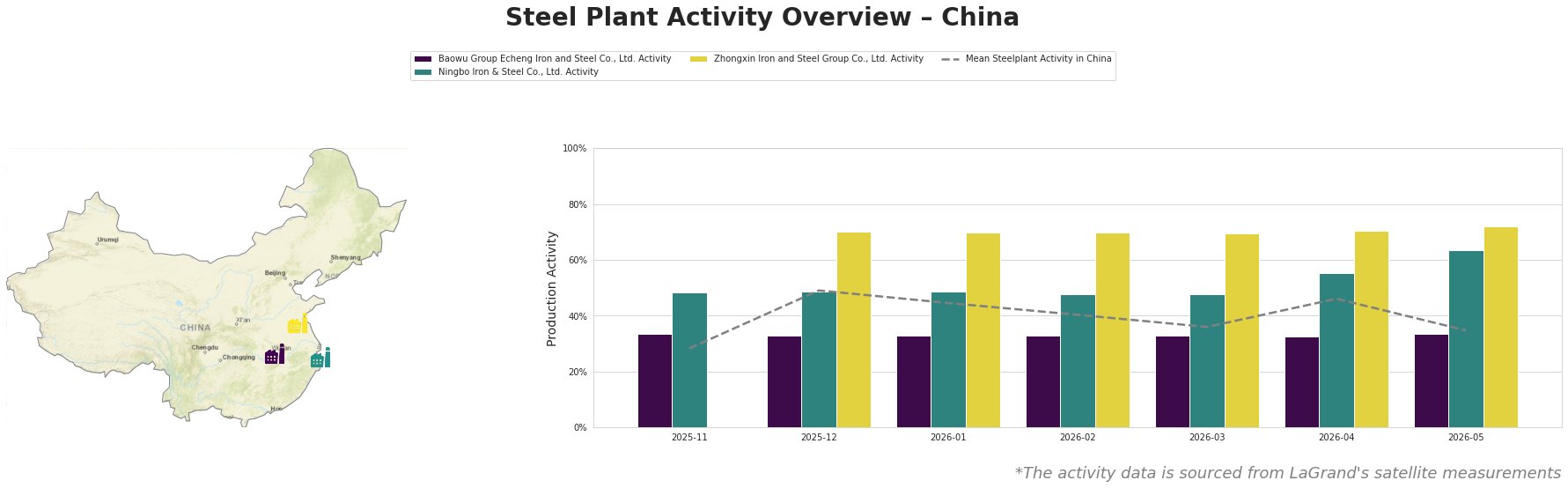

April 2026 saw a 3.5% dip in China’s crude steel output, aligning with satellite data showing mean steelplant activity dipping to 46% in April, down from 49% in March. Notably, Baowu Group Echeng Iron and Steel’s activity remained relatively stable at 33%, while both Ningbo Iron & Steel and Zhongxin Iron and Steel Group increased activity levels to 70% and 72%, respectively.

Baowu Group Echeng Iron and Steel Co., Ltd., located in Hubei, maintained a consistent activity level of 33%. Its production capacity remains significant, yet the ongoing reductions in output, highlighted by the April production figures, suggest potential supply constraints. There is no direct evidence connecting Baowu’s stable output to recent news, indicating its capacity may absorb fluctuations better than others.

In contrast, Ningbo Iron & Steel Co., Ltd. increased activities from 48% in March to 64% in May, signaling a recovery or enhanced operational capability, likely aiming to leverage market demand amidst broader reductions reported globally. The article “World steel production declines for eighth month with 2% drop in April” suggests that increased production from regions like Ningbo offers procurement opportunities.

Zhongxin Iron and Steel Group Co., Ltd. has also ramped up activity from 69% in March to 72% in May. This suggests readiness to meet potential upticks in demand and positions them favorably for procurement amid declining competitors.

The observed activity levels, coupled with production drops from “Global steel production fell by 4.1% m/m in April”, reflect a positive sentiment but emphasize the need for procurement strategies focused on stable suppliers like Ningbo and Zhongxin, potentially navigating disruptions stemming from Baowu.

Steel buyers should prioritize sourcing from relatively stabilized and resilient suppliers, adjust procurement schedules, and monitor the market’s evolving dynamics for timely adjustments to mitigate risk amidst structural industry changes.