From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineAsia Steel Market Update: Neutral Sentiment Amidst Declining Production and Weak Demand

China’s steel market faces downward pressure as indicated by major recent reports. Notably, China’s steel output fell by 4% y/y in January–April, reflecting sluggish demand exacerbated by a prolonged real estate crisis (2026-05-17). This trend is further affirmed by China’s crude steel output down 3.5 percent in April 2026, maintaining downtrend in Jan-Apr (2026-05-18), which aligns with satellite reconnaissance indicating a marked decrease in activity levels at key steel plants across Asia.

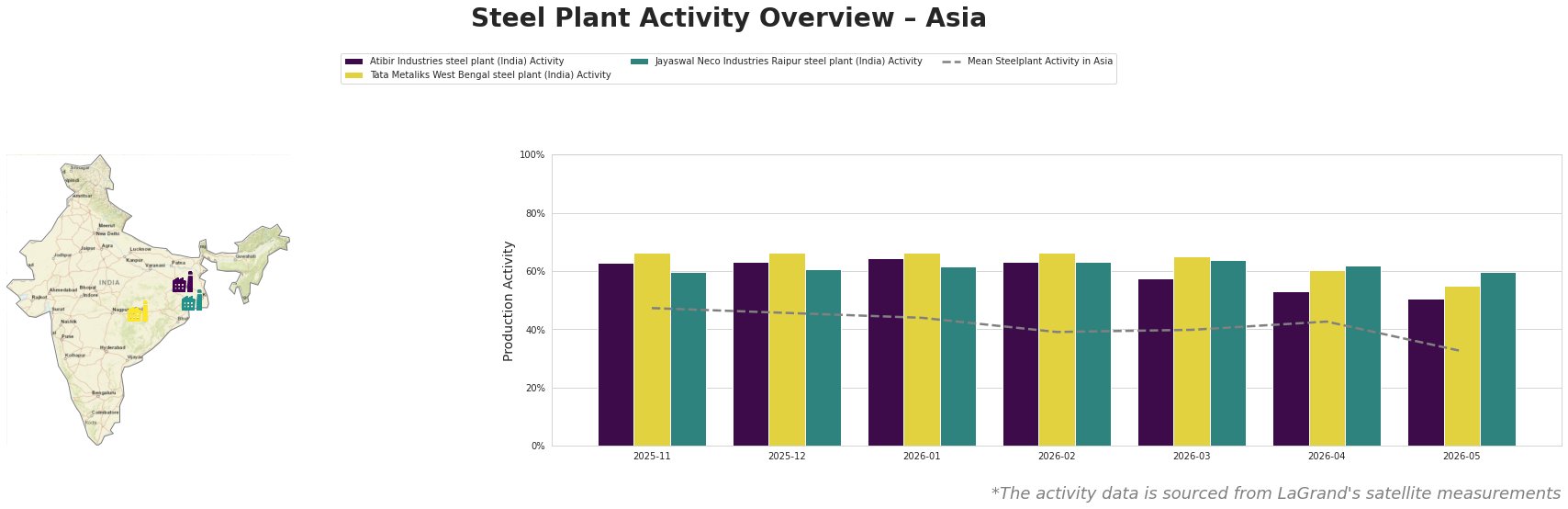

Measured Activity Overview

Activity levels across the observed steel plants have generally declined, particularly noted in the mean activity decrease from 47.0 to 33.0 between April and May 2026. Atibir Industries experienced a significant drop from 63.0 to 50.0, while Tata Metaliks showed a decrease from 60.0 to 55.0, aligning with diminishing production trends reported in Global steel production fell by 4.1% m/m in April (2026-05-21). The general market contraction illustrates ongoing weak end-user demand, with no direct correlation to strong recovery signals.

Plant Analysis

Atibir Industries, located in Jharkhand, produces primarily pig iron and rolled products through an integrated blast furnace (BF) setup. The plant’s activity saw a notable decline of 10% from April to May, dropping to 50%, which coincides with the reported 4% year-on-year decline in China’s steel output. This suggests a reactive adjustment to weakening domestic steel demand.

Tata Metaliks, situated in West Bengal and operating under similar integrated processes, maintained a moderate activity level but still registered a decline. Activity slumped from 60.0 in April to 55.0 in May. The decreases can be partially attributed to China reduced iron ore production by 1% y/y in January–April (2026-05-20), indicating possible upstream supply constraints affecting overall output dynamics.

Jayaswal Neco Industries, with a higher capacity of 1200 tons, also reflects downward activity movement from 62.0 to 60.0. This drop echoes the broader trend of global steel production declines, reinforcing the neutral market sentiment amid increasing competition and reduced export opportunities.

Evaluated Market Implications

The ongoing reduction in production levels across major Asian steel producers, particularly China, poses a substantial risk of supply shortages. The declines at plants like Tata Metaliks and Atibir Industries suggest a potential contraction in output that may lead to increased domestic prices if demand stabilizes. Steel buyers should consider immediate procurement due to the observed shifts—particularly at Atibir Industries and Tata Metaliks—highlighting recommendations for additional sourcing strategies before potential price increases materialize from further supply constraints.

In conclusion, the steel market sentiment remains neutral, but with pertinent shifts in production capacity and activity signals that warrant close monitoring while making informed sourcing decisions.