From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineUnfolding Challenges in the European Steel Market: Negative Sentiment Intensified by UK Import Quota Changes

In Europe, recent developments indicate a negative outlook for the steel market, primarily driven by significant concerns related to UK steel import quotas. The articles “BCC warns UK steel quota changes could disrupt supply chains“ and “British commerce chamber warns over steel quota damage“ highlight that proposed alterations to steel quotas and tariffs in the UK may drastically increase manufacturing costs and disrupt supply chains. These anticipated cost hikes align with drops in activity levels at key steel plants across Europe.

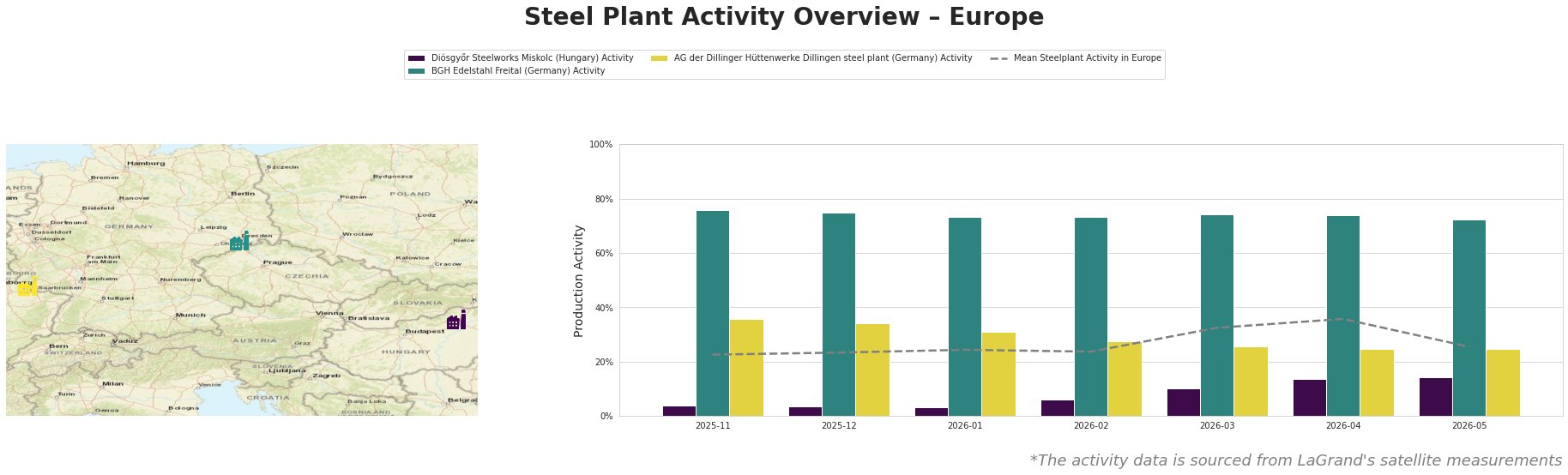

Overall, the average activity level dropped from 36% in April to 26% in May 2026, evidencing a negative trend. Diósgyőr Steelworks in Hungary saw a steady fall, dropping from 14% to 14%, which while stable, indicates only minimal recovery potential. Conversely, BGH Edelstahl Freital and AG der Dillinger Hüttenwerke experienced declines as well, with BGH’s activity decreasing by 4% and Dillinger’s by 1% during the same period.

At Diósgyőr Steelworks (Hungary), activity levels remained consistently low at 14%. The steel plant, largely focused on electric arc furnace production, seems susceptible to disruptions hinted at in the articles regarding UK steel supply chains. The ongoing uncertainty regarding quotas and tariffs may deter operations that rely heavily on imported materials. There is no direct link between their activity changes and Article references.

BGH Edelstahl Freital (Germany) specializes in stainless and tool steels with a current activity of 72%. The gradual decrease correlates with concerns described in the article “BCC warns UK steel quota changes could disrupt supply chains,” suggesting that disruptions leading to reduced demand and production practices are likely impacting this plant.

AG der Dillinger Hüttenwerke in Germany, with its integrated steel production capacity, saw activity drop to 25%. This facility might be affected not only by UK quota changes but also due to an overarching reduction in supply chain network reliability addressed in the articles.

Given these findings, steel buyers and analysts should anticipate potential disruptions in sourcing, particularly from Diósgyőr and Dillinger, where low activity levels could translate to supply shortages. To mitigate risks, it is advisable to secure contracts for critical steel requirements before any further quota restrictions are enforced, potentially seeking alternatives to UK and EU steel to ensure a steady supply line.