From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEuropean Steel Market Report: Current Trends and Future Outlook Pertaining to CBAM and Plant Activity

In Europe, the evolving dynamics of the steel sector are impacted significantly by the EU’s Carbon Border Adjustment Mechanism (CBAM) and new green steel standards. Recent articles such as “Green steel standards and CBAM reshape Turkish steel industry” and “Business associations have called on the EC to adopt a special CBAM approach for Ukraine” highlight the challenges posed by these regulations, while satellite data provides real-time insights into plant activities correlating with these developments.

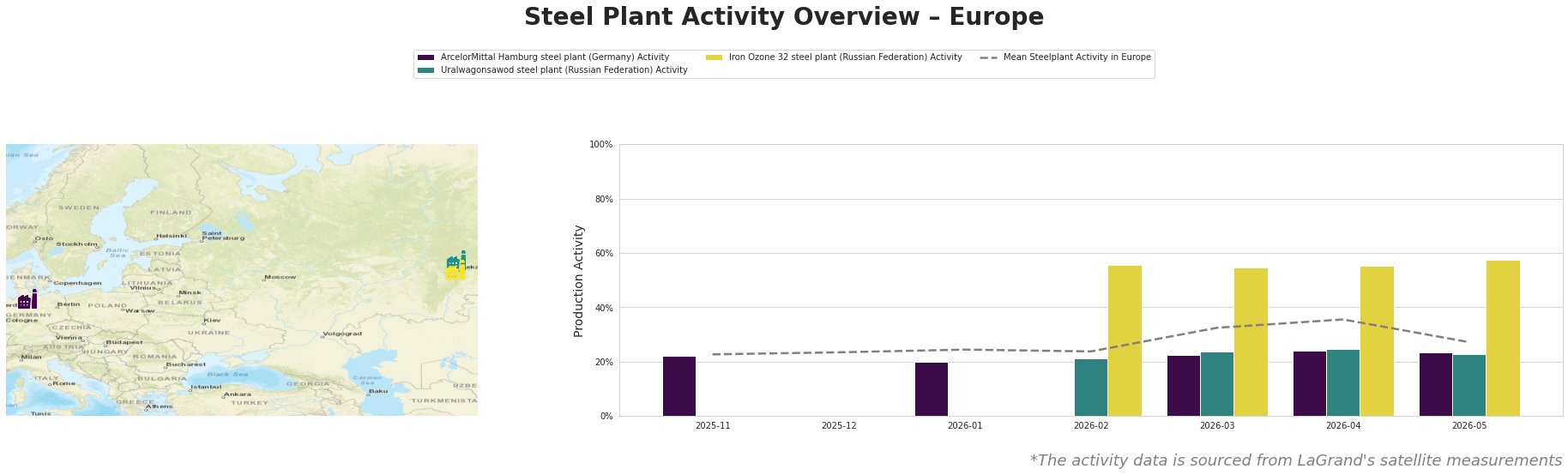

The ArcelorMittal Hamburg steel plant has seen a decline in activity, with a decrease to 20% in January, aligning with concerns raised in the article “Green steel standards and CBAM reshape Turkish steel industry,” emphasizing the challenges in adapting to new green criteria. The overall European mean activity reflects fluctuations, especially in early 2026.

In contrast, the Iron Ozone 32 steel plant exhibits a notable resilience with increased activity peaking at 57% in May, suggesting a robust production strategy amid burgeoning challenges tied to the CBAM implementation affecting the regional market. However, the Uralwagonsawod steel plant has also shown variability, reporting a decrease to 21% in February but stabilizing around 23% in May, suggesting potential supply instability as outlined in “Business associations have called on the EC to adopt a special CBAM approach for Ukraine.”

The differential performance between these plants indicates a disparity in operational readiness and adaptation strategies. Buyers should monitor ArcelorMittal’s adaptive measures closely in response to CBAM, while the rise at Iron Ozone offers potential procurement opportunities. Direct links to surveillance data suggest that local conditions for production resilience may still exist despite overarching regulatory pressure.

Potential supply disruptions may stem from stringent CBAM implications, particularly affecting Ukrainian steel producers unable to meet required emission standards amid existing geopolitical instability. Procurement specialists should, therefore, consider leveraging suppliers with proven adaptability and documented emission reductions to mitigate risks associated with the forthcoming operational and pricing uncertainties linked to the EU’s regulatory framework.