From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineNeutral Steel Market Outlook: EU Import Regulations and Activity Trends

Recent developments in Europe highlight adjustments in the steel import landscape alongside measurable plant activity fluctuations. The European Council’s announcement in The European Council describes in detail the amendments to the trade regime and the EU’s details in EU announces new steel import quota volumes and implementation changes reveal impending regulatory changes with a fresh total quota of 18.35 million metric tons effective July 1, 2026. These measures strive to manage global overcapacity and protection of local producers, aligning with observed satellite data trends from key plants.

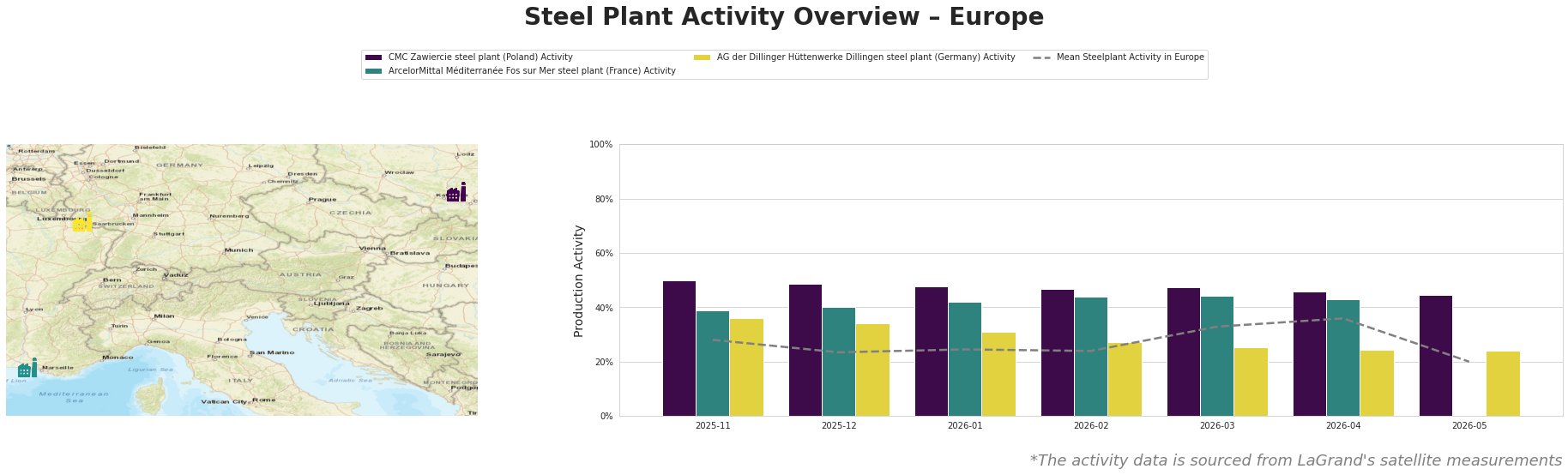

Over recent months, the CMC Zawiercie steel plant has maintained activity levels above the mean at 50% in November 2025, tapering only slightly to 45% by May 2026. It’s evident the upcoming import quota adjustments aim to help sustain this activity amidst regulatory pressures.

The ArcelorMittal Méditerranée Fos sur Mer plant witnessed a drop from 40% to only 24% activity by May 2026, with no production reported at the end of that month. This downward trend aligns with EU intentions to curtail external steel dependency, particularly against the backdrop of rising tariffs on oversupplied materials. Such regulation changes set the stage for potential strain on production capabilities.

The AG der Dillinger Hüttenwerke Dillingen plant similarly reported a decline in activity from 36% to 24% since April 2026 without a substantial recovery forecast. There’s a notable alignment with the news regarding possible supply disruptions tied to stricter import tariffs.

Given these developments, potential supply disruptions could arise particularly for the ArcelorMittal plant due to the new regulations leading to restricted imports. Steel buyers should prioritize procurement from stable plants like CMC Zawiercie to mitigate risks associated with tariffs and reduced production capabilities at other facilities. Engaging with suppliers for timely deliveries of products defined under quota will be crucial in navigating these changes effectively while keeping track of future market developments tied to the ongoing regulatory landscape.