From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineDeclining Demand and Rising Costs Drive Negative Sentiment in Asia’s Steel Market

Recent developments in Asia’s steel market highlight substantial challenges for steel buyers, particularly in Turkey. According to “Murat Eryılmaz: Turkish steel sector faces weak demand and high costs”, the Turkish steel industry grapples with declining production due to weak domestic demand and export difficulties resulting from the Carbon Border Adjustment Mechanism (CBAM). Satellite data confirms a marked decrease in activity levels among key steel plants in the region, illustrating the broader trend of contraction.

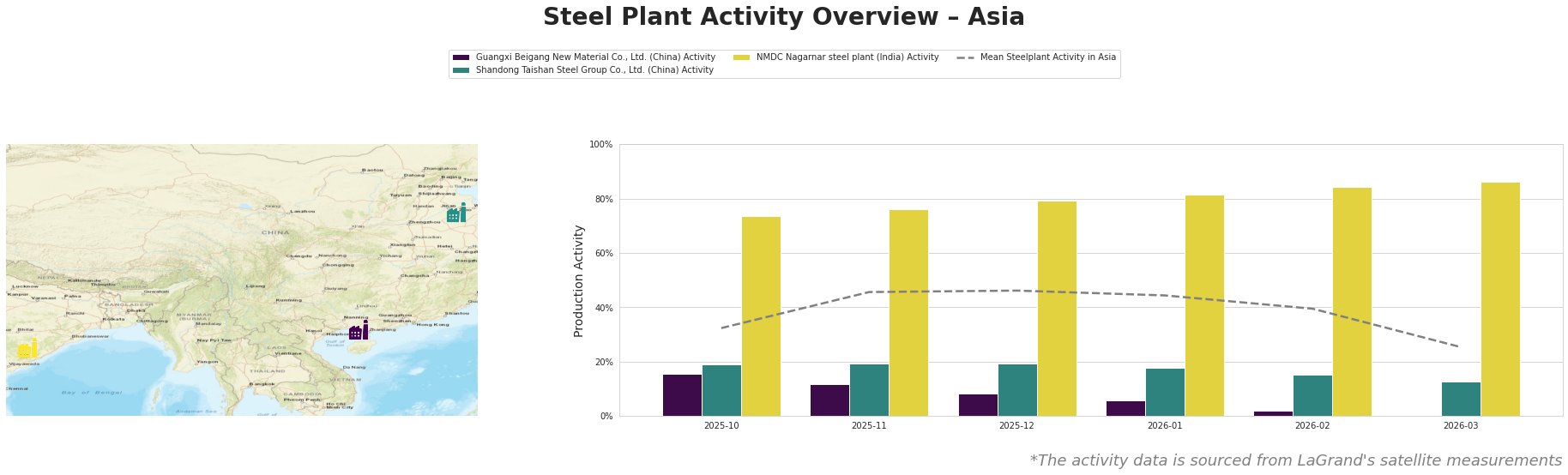

Across the observed steel plants in Asia, activity levels have notably declined, with Guangxi Beigang New Material Co., Ltd. reaching a historic low of 0.0% in March 2026. This is in stark contrast to NMDC Nagarnar’s relatively higher output, reaching 86.0%. The downturn in Guangxi, which correlated with findings from “Murat Eryılmaz: Turkish steel sector faces weak demand and high costs”, illustrates that the Turkish sector’s overall challenges are reflected in declines across regional operations.

Guangxi Beigang experienced a consistent decrease from 15.0% in October 2025 to 0.0% by March 2026, emphasizing its struggle amidst rising costs and weak demand, though no direct connection was established to the Turkish context. Shandong Taishan’s activity faltered from 19.0% to 13.0% during this period, showcasing drops that align with pressures outlined in Eryılmaz’s reports.

NMDC Nagarnar steel plant maintained higher utilization, reaching 86.0%, though the overall market sentiment suggested an impending vulnerability to demand fluctuations as indicated in Eryılmaz’s statements about weak domestic consumption and export issues.

The amalgamation of these challenges suggests potential supply disruptions, especially for Turkish exporters and their dependency on external markets under increased global protectionism as reported. Steel buyers should consider tightening procurement schedules and leveraging existing relationships with higher-performing plants like NMDC to mitigate risks associated with reduced supply.

In conclusion, steel procurement professionals should brace for continued price pressures and potential supply shortages, emphasizing the need for agile purchasing strategies that account for the weakening sentiment permeating the region’s steel market.