From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEuropean Steel Market Outlook: Strong Domestic Demand Amidst Quota-Driven Price Surges

Europe’s steel market is seeing a Very Positive trend due to robust domestic demand and significant changes driven by recent governmental interventions, particularly in the UK. The articles “European coil and green steel round-up: EU coil prices continue upward trend as costs and import barriers bite“ and “UK HRC prices likely to surge on quota plan: sources“ elucidate the region’s current climate, indicating upward pressure on hot-rolled coil (HRC) prices largely influenced by reduced import quotas and rising domestic prices.

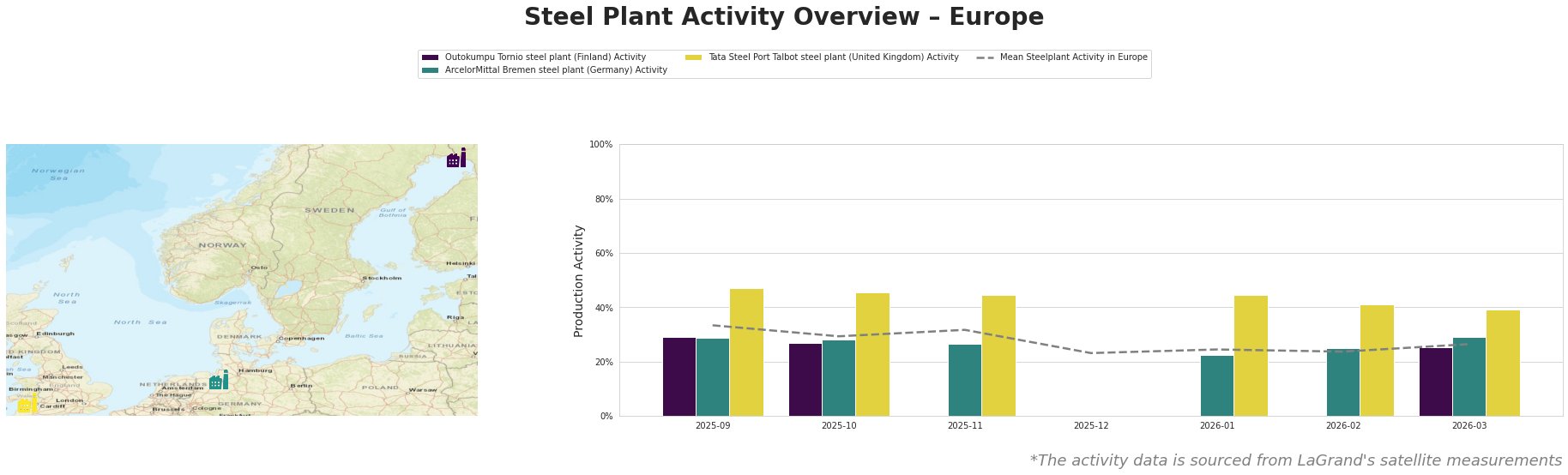

Satellite data indicates an uptick in activity levels across certain plants, with notable month-on-month improvements. However, the ArcelorMittal Bremen steel plant remains at 29% activity, conforming closely to the average across Europe. Notably, Tata Steel Port Talbot shows a slight decline to 39%, reflecting cautious buyer sentiment due to ample existing stock, corroborated by “European HRC price momentum slows amid limited demand.” Outokumpu Tornio, on the other hand, registered 25% activity, aligning with a broader trend towards prioritizing domestic production amid higher energy costs and logistics issues.

In detail, Outokumpu Tornio has seen recent activity stabilize around 25%, aligning with increasing domestic prices, as noted in the “European coil and green steel round-up” emphasizing limited imports. ArcelorMittal Bremen, despite recent stabilization, remains under relative capacity with operational dynamics that favor robust production primarily focused on HRC and CRC. The Tata Steel Port Talbot experienced a slight decrease in activity, suggesting a cautious approach from buyers who have sufficient stock levels, tying back to sentiments expressed in the “European HRC price momentum slows amid limited demand.”

The implications of a proposed reduction in UK quotas, as detailed in the “UK HRC prices likely to surge on quota plan: sources,” signal potential shortages that might elevate prices beyond current projections, thereby pushing European mills to adjust pricing strategies to remain competitive.

Recommendations for Steel Buyers:

- Prioritize Domestic Sourcing: Given the limited import options and rising freight costs, buyers should focus on securing contracts with domestic suppliers to mitigate risks associated with potential shortages and price escalations.

- Monitor UK Quota Changes: Stay updated on upcoming UK government proposals regarding import quotas, as this might create sudden spikes in demand for specific product grades from EU suppliers.

- Adjust Procurement Strategies: Focus on immediate procurement of HRC and HDG over CRC due to increased prioritization by mills, capitalizing on current domestic price advantages before anticipated further increases take place.

By aligning procurement strategies with these actionable insights, buyers can navigate the evolving market landscape effectively while mitigating supply chain risks.