From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineAsia’s Steel Market Outlook: Robust Growth Fueled by Strategic Plant Activity and Production Gains

Recent data from Asia highlights a significant upward trend in steel production, aligning with developments in major regional plants. As noted in the article “Global DRI output up 11.5 percent in January 2026,” the surge in global direct reduced iron production correlates with heightened activity across Asian facilities, indicating a very positive sentiment in the steel market.

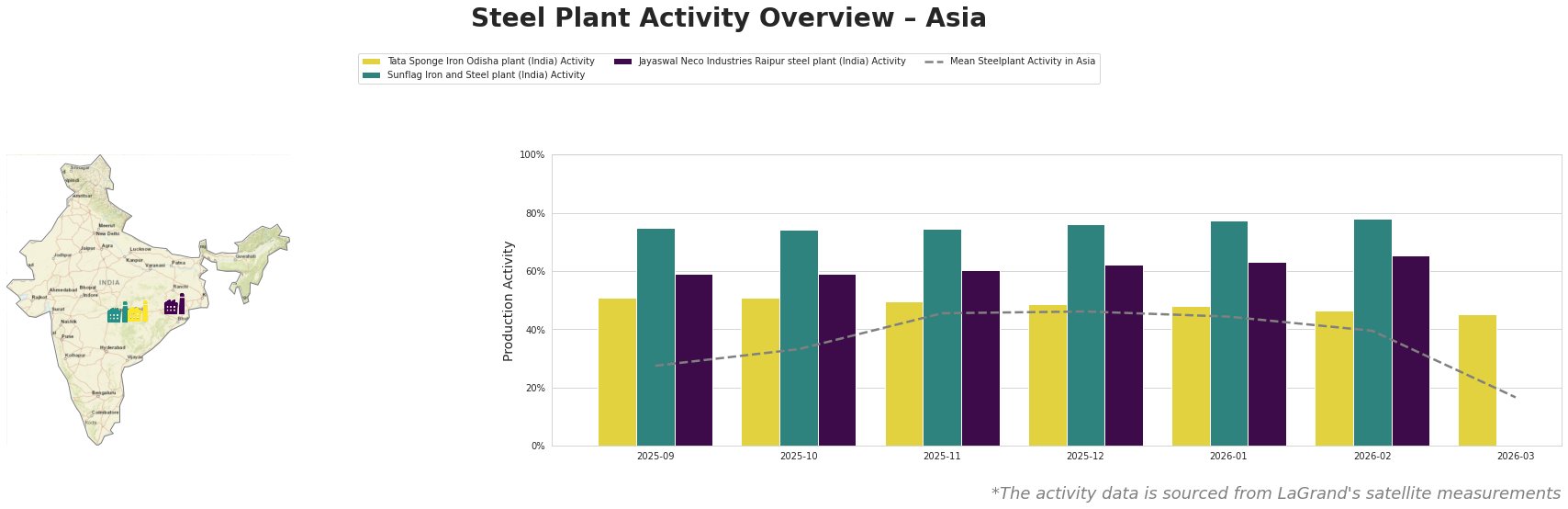

In January, the Sunflag Iron and Steel plant in Maharashtra exhibited strong activity at 78.0%, significantly above the mean Asian steelplant activity of 40.0%, reflecting a 16% increase from December 2025. This aligns with the growth in Asian stainless steel production, reported in the article “Global stainless steel production in 2025 grew by 2.1% y/y,” where China’s leading output contributed notably, demonstrating a solid demand for stainless products.

Conversely, the Tata Sponge Iron Odisha plant registered a decline in activity to 46.0% for February 2026, down from 49.0% in December 2025, despite being a vital contributor to the DRI production surge highlighted in the DRI output article. Activity at the Jayaswal Neco Industries Raipur steel plant also fell to 63.0%, with no recent connections established to the cited news articles, implying strategic retrenchment as market conditions fine-tune.

Elevated activity levels in Sunflag Iron and Steel point towards robust demand—likely influencing pricing structures and availability in the near term. In contrast, the pullback in activity at Tata Sponge Iron Odisha and Jayaswal Neco plants indicate potential short-term supply disruptions in the DRI and integrated steel product segments.

Buyers should consider strategic procurement shifts, capitalizing on Sunflag’s output strength, while monitoring Tata and Jayaswal’s activity to mitigate risks of supply gaps. The competitive pricing resulting from increased yield in U.S. steel production—as noted in discussions on tariffs—also provides an opportunity for Asian buyers to cost-effectively optimize their sourcing strategies. The overall market sentiment remains very positive, supported by strong regional outputs and strategic plant performances.