From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineAsia Steel Market Shrinks Amid Global LNG Price Surge: Severe Implications for Buyers

The steel market in Asia is currently facing a very negative sentiment primarily driven by external geopolitical tensions that are affecting raw material prices. Recent articles such as “European gas prices are rising rapidly amid escalation in the Middle East“ and “US LNG margins soar on Hormuz disruption“ highlight how escalating conflict in the Middle East has dramatically increased global LNG prices, thereby affecting raw material costs for steel production. Observations from satellite data indicate significant drops in activity levels at key steel plants in Asia, further worsening an already shaky market landscape.

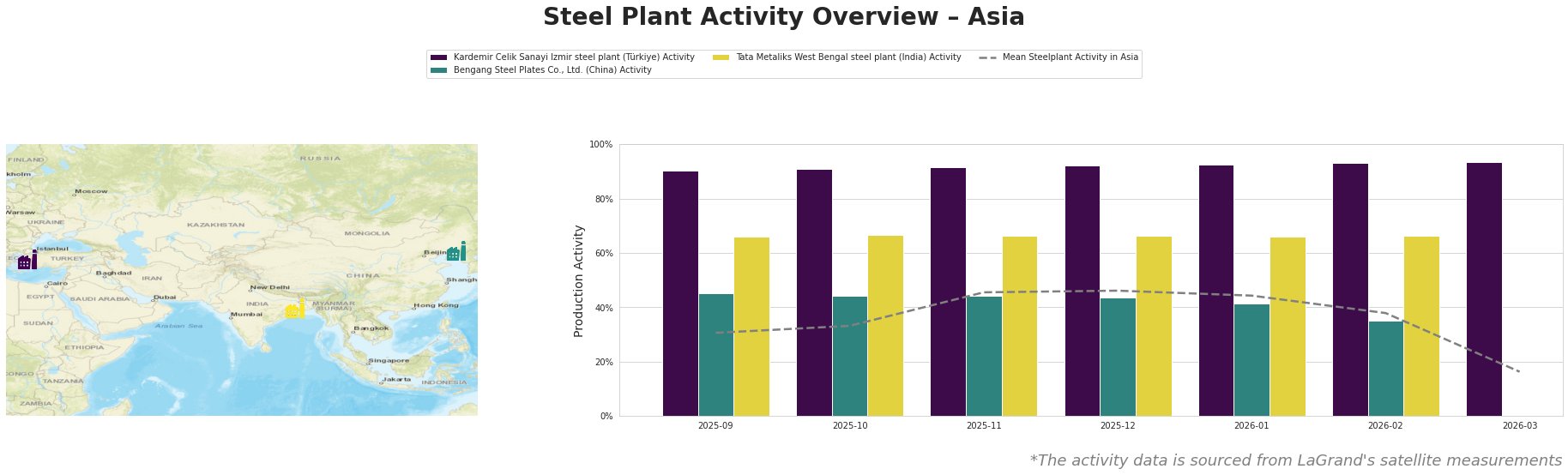

Activity levels across Asia’s steel plants plummeted, with the mean activity reaching a mere 16.0% by March 31, 2026. Notably, Kardemir Celik Sanayi Izmir maintained activity at 93.0%, yet this comes with heavy reliance on electric arc furnace (EAF) technology, illustrating that while some plants could sustain operations, the overall environment is starkly constricted. In contrast, Bengang Steel experienced diminished activity levels, but due to insufficient data reported, precise impacts from recent events cannot be fully established.

At Tata Metaliks, which focuses on pig iron and ductile pipes, the drastic drop in activity this month raises concerns about its capability to respond to tight market conditions influenced by increased LNG prices as discussed in “US LNG margins soar on Hormuz disruption”.

The implications of these trends are manifold. Ongoing disruptions in LNG supply, following disruptions in the Strait of Hormuz, correlate with increasing operational costs at steel plants due to rising energy prices. As highlighted in “European gas prices are rising rapidly amid escalation in the Middle East,” domestic steel producers facing higher costs may curtail output or delay orders, straining supply chains globally.

For procurement professionals, it is critical to consider the following:

– Prioritize partnerships with producers demonstrating higher activity levels like Kardemir, despite the market constraints.

– Anticipate potential supply shortages, particularly from plants like Tata Metaliks due to reduced capacity and higher operational costs.

– Explore alternative raw material sources beyond traditional suppliers, particularly in light of the unstable geopolitical situation affecting LNG prices.

Failure to adapt to these market dynamics may result in significant procurement challenges later in 2026 as production capacities struggle to realign with fluctuating demand.