From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEuropean Steel Market Report: Activity Declines Amidst Price Hikes and Weak Demand

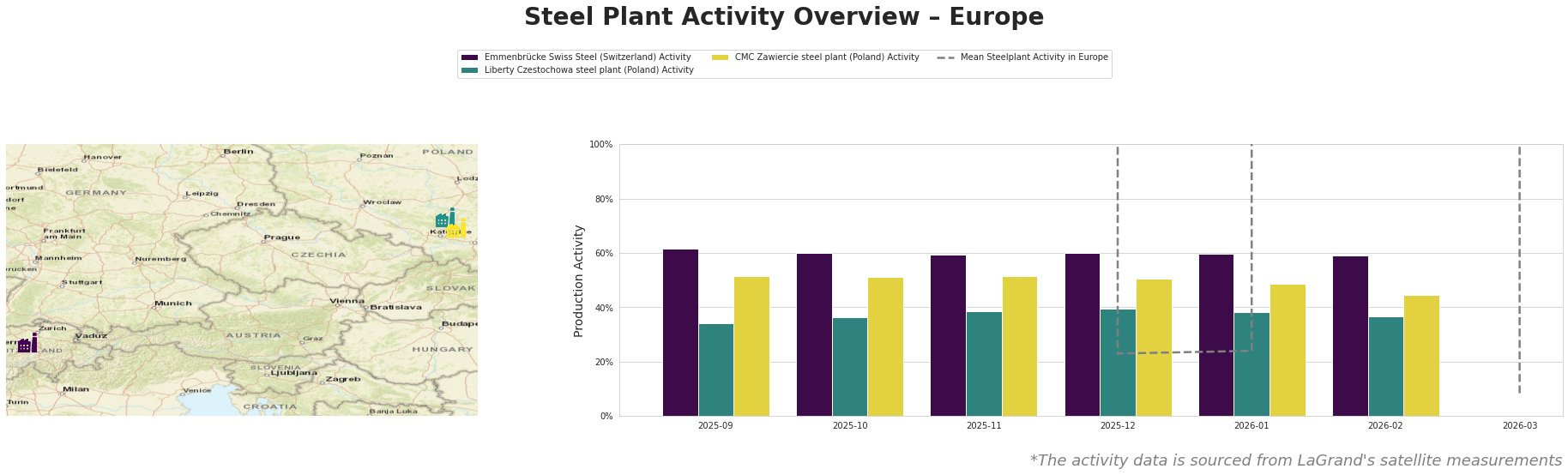

Recent developments in the European steel market highlight a troubling trend of declining activity levels at key plants, correlating with weak demand despite price hikes. Articles such as “Distributors slow to capitalise on EU coil hikes“ and “European HRC prices driven higher by restocking amid concerns over imports“ illustrate the disconnect between price increases and actual buyer engagement, evidenced by satellite activity data from major plants.

Emmenbrücke Swiss Steel has seen stable activity at 60–62%, but significant drops are noted in the overall average steelplant activity, plummeting to 8% by March 2026. These declines are notably aligned with the growing concerns from the article “European HRC prices driven higher by restocking amid concerns over imports”, which emphasizes weak end demand and apprehension regarding heightened costs linked to geopolitical tensions.

Liberty Czestochowa exhibited significant fluctuations with activity falling to 34% in September before stabilizing around 36-40%, while CMC Zawiercie experienced a decrease from 52% to 45% in the same timeframe. Increased import activity discussed in “Coil imports resurface in Italy“ demonstrates a need for cautious procurement strategies, as demand remains volatile and pricing dynamics shift unpredictably.

Emmenbrücke Swiss Steel, leveraging EAF technology, maintains stable operations despite market pressures, whereas Liberty Czestochowa and CMC Zawiercie show heightened sensitivity to the price mechanisms underscored by disruptions in steel supply chains post-Tata Steel UK’s furnace closure, as indicated by “UK HRC discount to north EU expands“.

The prevailing sentiment suggests that buyers should prioritize sourcing from stable regions or suppliers, especially given the potential for rising costs fueled by the EU’s Carbon Border Adjustment Mechanism, as described in “Coil imports resurface in Italy.” Given the tightening market landscape, procurement professionals are advised to hedge against future price fluctuations by engaging with lower-cost options from UK producers while remaining alert to associated import risks.

In summary, supply disruptions and the sharp divergence between price hikes and actual demand require immediate attention from steel buyers seeking to navigate this challenging environment.