From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EnginePositive Steel Market Outlook for Europe Driven by Automotive Recovery

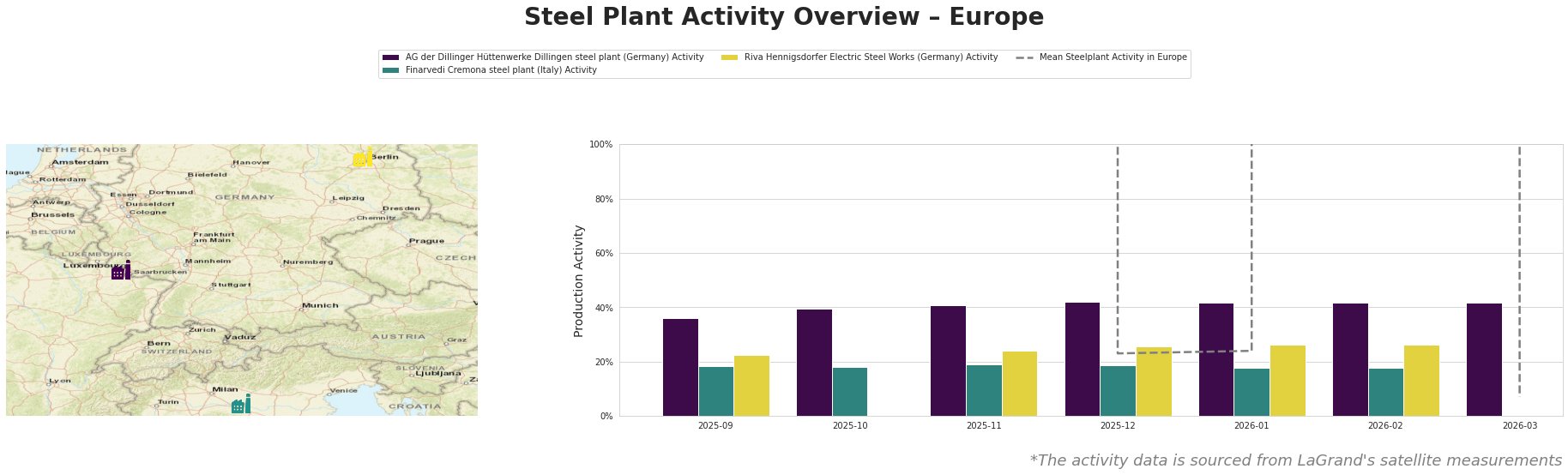

Spain’s automotive recovery is positively influencing Europe’s steel market, highlighted by the articles “Spain’s car sector recovers in January“ and “Spain’s automotive sector rebounds in January.” This recovery is reflected by sustained activity levels from major steel plants, particularly AG der Dillinger Hüttenwerke, which has consistently operated at 42% capacity in January and February 2026 amidst a generally favorable market sentiment. Notably, while some plants have shown stable trends, overall activity remains closely tied to automotive demand fluctuations, especially given declining registrations highlighted in the article “New car registrations in EU down 3.9 percent in Jan 2026.”

The AG der Dillinger Hüttenwerke has remained stable, reflecting solid demand for semi-finished and finished rolled steel vital for automotive and infrastructure sectors. Continuous operation at 42% aligns with improved production in Spain’s automotive sector despite broader regional uncertainties.

Finarvedi Cremona has maintained significantly lower activity levels (18% in the last two months), indicating a localized impact from softening demand in Europe’s automotive markets, as articulated in the aforementioned articles regarding the decline in German and French markets.

Meanwhile, Riva Hennigsdorfer Electric Steel Works has consistently operated at 26%. The connection to the automotive market is reinforced by the recent upsurge in automotive production in Spain. However, no new distinctions were identified to specifically correlate their output with the current activity shifts.

Given the robust recovery in Spain’s car production, steel buyers should advise procurement strategies that emphasize securing supplies from AG der Dillinger Hüttenwerke, which shows resilience and capacity to meet demand. Additionally, while considering the Finarvedi Cremona site, buyers must prepare for possible disruptions if nearby automotive demand does not stabilize, aligning with José López-Tafall’s caution on future production impacts.

In summary, while the overall sentiment is positive, strategic procurement actions should focus on maintaining close monitoring of the automotive industry’s health in key German and French markets to mitigate potential supply disruptions in the broader European steel market.