From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEuropean Steel Market Analysis: Impacts of UK Quota Changes and Plant Activity Trends

Recent developments in the European steel industry highlight a neutral market sentiment amid shifting regulatory frameworks and fluctuating steel plant activity levels across the continent. The recent articles UK to remove Turkish HDG quota exemption and UK to cancel Turkey’s exemption from HDG quotas have directly linked increased Turkish steel imports to the UK’s changing import regulations, as Turkey’s HDG products will now be subject to stricter quotas beginning April 1, 2026. However, no direct correlations between these regulatory changes and observed activity levels at European plants have been established.

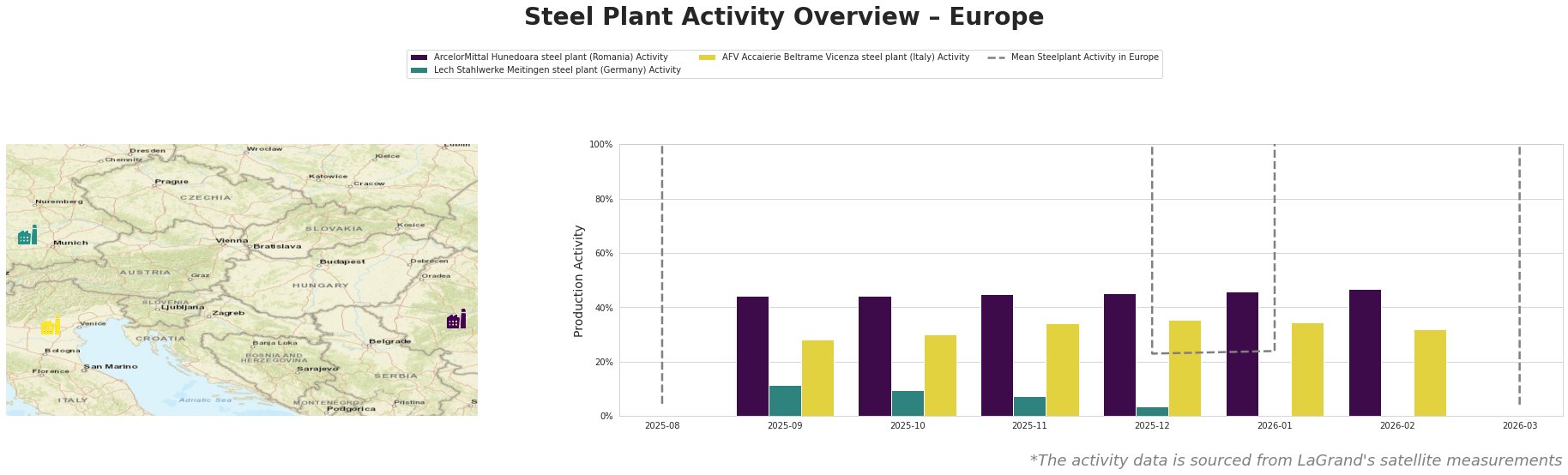

ArcelorMittal Hunedoara, with a capacity of 800, primarily utilizing Electric Arc Furnace (EAF) technology, exhibited a gradual increase in activity from 44% to 47% over several months, aligning with a broader demand stabilization despite being influenced indirectly by Turkish market shifts. Conversely, Lech Stahlwerke Meitingen showed a stark decline, dropping to 0% by January 2026, showcasing severe operational pauses, potentially tied to changing export dynamics and buyer preferences. While the firm’s activities started at 11% in September 2025, they fell continuously, indicating vulnerabilities associated with competitive pressures likely exacerbated by the impending quota transitions on Turkish imports. AFV Accaierie Beltrame Vicenza experienced minimal fluctuation, maintaining activity between 30% and 35%, signaling a relatively stable operational environment unperturbed by the recent regulatory changes.

Given these developments, potential supply disruptions are evident, particularly with Lech Stahlwerke Meitingen’s stark decrease in productivity, which may impede timely sourcing of steel products essential for construction and infrastructural renewal projects. Steel buyers are advised to diversify procurement sources and maintain stockpiles, especially for rolled products which may face scarcity due to regulatory ripples. Furthermore, buyers should closely monitor developments regarding Turkey’s market access to reassess supplier strategies, as these regulatory shifts may disrupt supply chains reliant upon Turkish exports.

In summary, while the implications of UK regulatory shifts are notable, the observable activity trends across European steel plants reveal critical vulnerabilities and necessitate proactive procurement strategies to mitigate supply risks.