From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEurope Steel Market Analysis: Activity Dips Amid Plant Shutdowns, Neutral Sentiment Prevails

Recent developments in Europe’s steel market are dominated by significant operational challenges faced by key producers, particularly in Spain and Italy. ArcelorMittal’s announcement to halt blast furnace in Spain for ‘several months’ directly correlates with a notable drop in activity levels at the Aviles and Gijón plants. Moreover, Italian steelmaker Acciaierie d’Italia’s plan to increase steel production to 4 million tons per year amid government-led restructuring contrasts with ongoing disruptions, yet activity recovery remains to be seen.

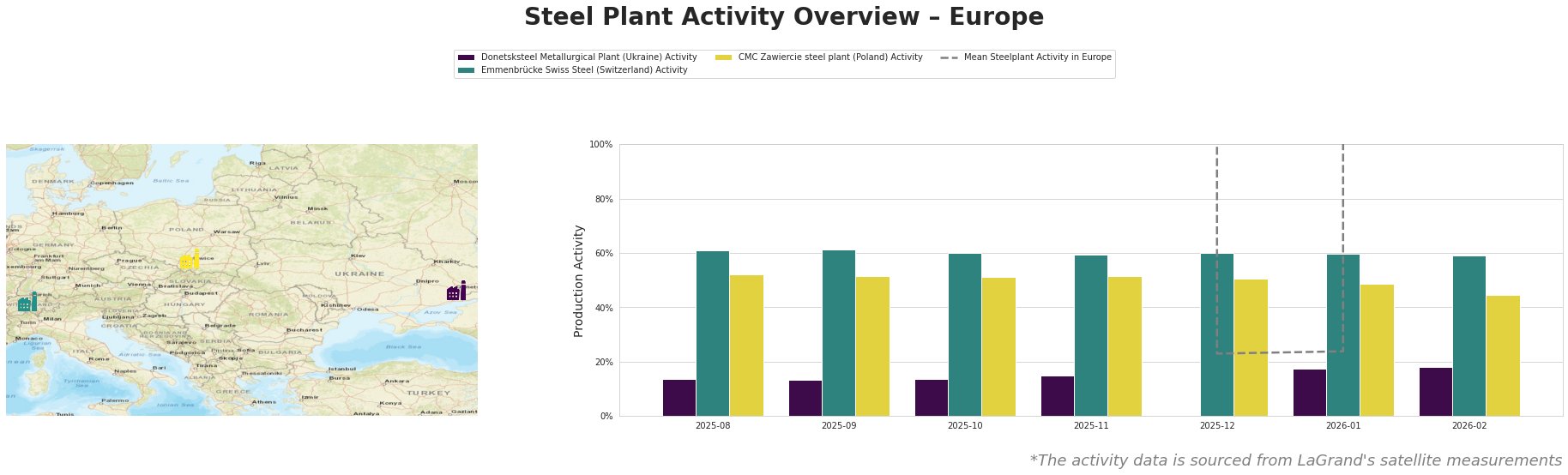

Donetsksteel has maintained consistent low activity levels, with only 14% in August 2025, increasing to 18% by February 2026. No direct correlation between the shutdowns and Donetsksteel’s activity can be established. Emmenbrücke’s activity remained stable around 60%, highlighting its operational resilience. CMC Zawiercie, however, experienced a gradual decline, dropping from 52% in August to 45% in February 2026, suggesting potential market pressures despite no direct linking news articles.

ArcelorMittal’s activities have been particularly affected, with recent information from ArcelorMittal temporarily shuts down blast furnace B in Gijón and ArcelorMittal temporarily shuts down BF in Spain indicating reduced capacities at both the Gijón and Aviles locations, which limited supply. This aligns with activity data indicating significant operational challenges. The decision to idle blast furnace B in Spain is anticipated to disrupt supplies of pig iron, compelling ArcelorMittal to increase imports from elsewhere.

In contrast, Acciaierie d’Italia, with plans to revive production to 4 million tons per year, seeks to recover from below-target outputs driven by earlier shutdowns and restructuring issues. This ambition stems from governmental intervention, aiming to stabilize supply chains.

Market Implications

Steel buyers should closely monitor ArcelorMittal’s blast furnace operations due to the potential supply disruptions caused by these extended shutdowns, particularly in Spain. Immediate procurement actions should focus on sourcing alternatives to mitigate risks, especially as the Gijón plant is projected to remain offline for the next several months. For clients relying on intermediate products during this period, alternative suppliers or increased stockpiling may be advisable.

Given the ambitious ramp-up plans of Acciaierie d’Italia, procurement strategies should also consider the potential for increased supply from Italy, contingent upon successful execution of their restructuring strategy. However, the uncertainty regarding their operational continuity still necessitates a cautious approach.

Overall, the current sentiment within the European steel market remains Neutral, with static activity levels signaling a need for strategic sourcing aligned with evolving operational realities across the region’s key production facilities.