From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EnginePositive Steel Market Outlook for Ukraine: Addressing Supply Dynamics Amid Export Challenges

Ukraine’s steel sector is facing significant shifts, driven by regional export challenges and fluctuating consumption patterns. Recent reports such as “Iron ore exports from Ukraine have collapsed: China is reducing purchases” and “Ukraine reduced pig iron exports by 27% y/y in January” indicate a marked decline in steel-related exports and a complex interplay of factors affecting local production activities.

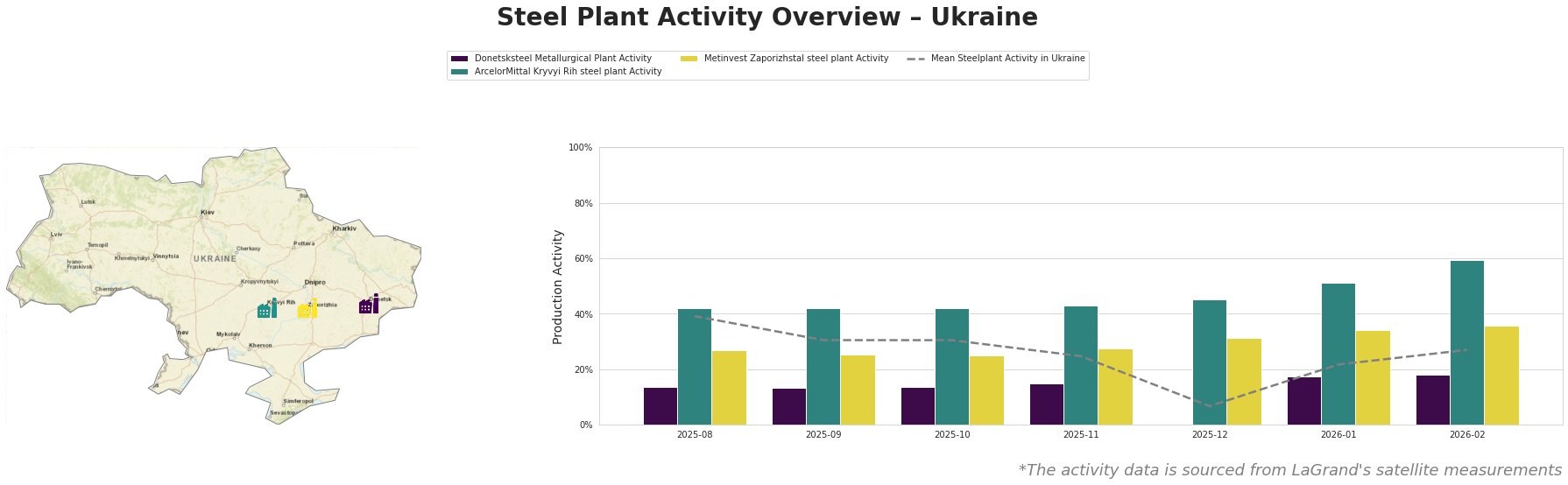

In January 2026, pig iron exports plummeted by 27.1% y/y, totaling 93.79 thousand tons, driven by diminished demand from key markets such as the U.S. and Italy. This decline aligns with reduced operational activity visible through satellite data, which shows a rebound in output at the ArcelorMittal Kryvyi Rih steel plant to 51%—higher than the mean activity of 22% in January. However, Donetsksteel remains underutilized at 17%, particularly as observed shifts in pig iron exports could further influence its production viability, without a direct link to export performance established.

The ArcelorMittal Kryvyi Rih steel plant has demonstrated resilience, increasing to 59% activity in February 2026. This improvement is substantiated by its capacity to adapt within integrated production processes despite facing export downturns, aligning with reduced pig iron exports. In contrast, the Metinvest Zaporizhstal steel plant showcases stable performance, reflecting the overall recovery trend in the market as it navigates through external pressures.

The scrap export crisis, noted in “Scrap exports from Ukraine amounted to 9.3 thousand tons in January,” further complicates the situation with significant declines observed. A 40.7% y/y drop hampers reprocessing efforts crucial for steel production, as domestic demands rise amid regulatory support.

In this context, steel buyers should focus on forging partnerships with facilities exhibiting robust production capabilities, like ArcelorMittal, while staying abreast of evolving export conditions to mitigate potential supply disruptions linked with Donetsksteel’s low operating levels. Recommended procurement actions include:

- Prioritizing direct purchase contracts with ArcelorMittal Kryvyi Rih as production volumes are likely to remain favorable.

- Monitoring export trajectories from Ukrainian plants; transition to alternative suppliers if local plants fail to achieve consistent operational thresholds.

- Considering increased domestic sourcing for scrap metals in light of restrictions to bolster local supply chains.

Careful navigation of these evolving market dynamics lays the groundwork for strategic procurement decisions while addressing emerging supply constraints marked by ongoing geopolitical conditions.