From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineSouth America Steel: Import Quota Pressure Amid Production Dip, Freight Rate Hike

Brazil’s steel market faces a complex situation with rising import freight rates and domestic production declines, potentially impacting procurement strategies. “Freight rates increase slightly in July 2025 for Brazilian finished steel imports” highlights increased import costs, while “Brazilian crude steel production declined in July 2025” indicates potential domestic supply constraints. Though both articles highlight challenges, there is no direct relationship explicitly made between them. Observed plant activity changes, however, provide further context.

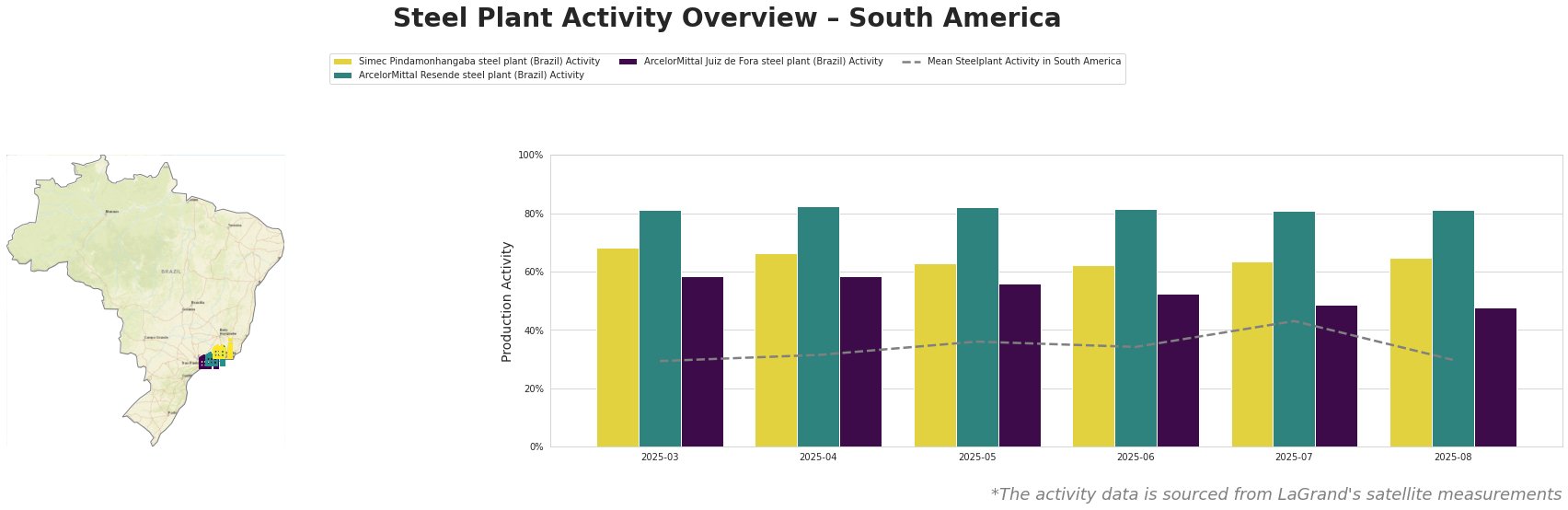

The mean steel plant activity in South America shows a rise to a peak of 43% in July, dropping back to 30% in August. Simec Pindamonhangaba has shown relatively consistent activity in the 60s, though it dropped to 62% in June. ArcelorMittal Resende displays consistently high activity, remaining stable at approximately 81-82% throughout the period. ArcelorMittal Juiz de Fora consistently shows the lowest activity levels of the observed plants, with a steady decline from 58% in March/April to 48% in August. This drop coincides with the reported decrease in Brazilian crude steel production, but a direct causal link cannot be explicitly established from the provided information.

Simec Pindamonhangaba, a 500 ttpa EAF-based plant in São Paulo producing wire rod and rebar for the building and infrastructure sectors, showed relatively stable activity levels from March to August, operating consistently above the South American average. The observed activity levels do not have any explicit relationship to the information in the provided news articles.

ArcelorMittal Resende, a 1000 ttpa EAF-based plant in Rio de Janeiro producing rebar and wire rod for various sectors, demonstrated consistently high activity near 81-82% throughout the observed period. Its continuous operation doesn’t directly correlate with any of the news articles, which mainly address broader market trends and not specific plant events.

ArcelorMittal Juiz de Fora, a 1100 ttpa integrated (BF & EAF) plant in Minas Gerais producing rebar, wire rod, and bars, has seen a gradual decline in activity from 58% in March/April to 48% in August. This trend aligns with the “Brazilian crude steel production declined in July 2025” announcement, though a definitive cause-and-effect relationship cannot be explicitly proven based solely on the provided materials.

“Brazil updates utilization of steel import quotas” reports a 68% utilization of import quotas. Simultaneously, “Brazilian crude steel production declined in July 2025” indicates a potential tightening of domestic supply. Given these factors, and considering the freight rate increase reported in “Freight rates increase slightly in July 2025 for Brazilian finished steel imports”, steel buyers should:

- Prioritize securing domestic supply contracts, particularly for products similar to those produced by ArcelorMittal Juiz de Fora (rebar, wire rod, bars), given its observed activity decline and the overall drop in Brazilian crude steel production, to mitigate potential shortages.

- Expedite import processes within the quota limits, particularly for products with high quota utilization rates such as galvalume (69%) and zinc coated (60%) steel, to avoid the 25% tax on exceeding the quotas.

- Factor increased freight costs into import calculations, especially when sourcing HRC from China, where freight rates reached $57/mt in July 2025, to accurately assess the total cost of imported steel.